Best Crypto Card UK 2026: 7 Cards Tested + HMRC CGT Rules

Quick answer: Best crypto cards for UK residents in 2026 are Gnosis Pay (self-custody, EEA+UK, up to 5% GNO cashback), MetaMask Card (self-custody, Feb 2026 UK launch via Baanx), and Wirex (FCA-registered, GBP IBAN included, multi-currency). The Jan 2026 HMRC Cryptoasset Reporting Framework now mandates UK platforms to share transaction data with HMRC. Every crypto-to-GBP tap is a CGT disposal; the Annual Exempt Amount is £3,000 (reduced).

The UK shifted regulatory gear in 2026. January saw the Cryptoasset Reporting Framework take effect — UK-based crypto platforms now report customer transaction data to HMRC. February saw the FCA name Revolut, Visa, Coinbase, and one other firm as approved stablecoin testers as part of the broader stablecoin regime due to finalise in late 2026. The practical upshot for UK crypto card users: regulated rails are increasingly the only rails, and HMRC tax compliance is no longer optional.

This guide covers the 7 crypto cards confirmed available to UK residents in May 2026, the HMRC CGT rules in detail, the FCA-registration status of each card's issuing partner, and the practical funding paths from major UK banks.

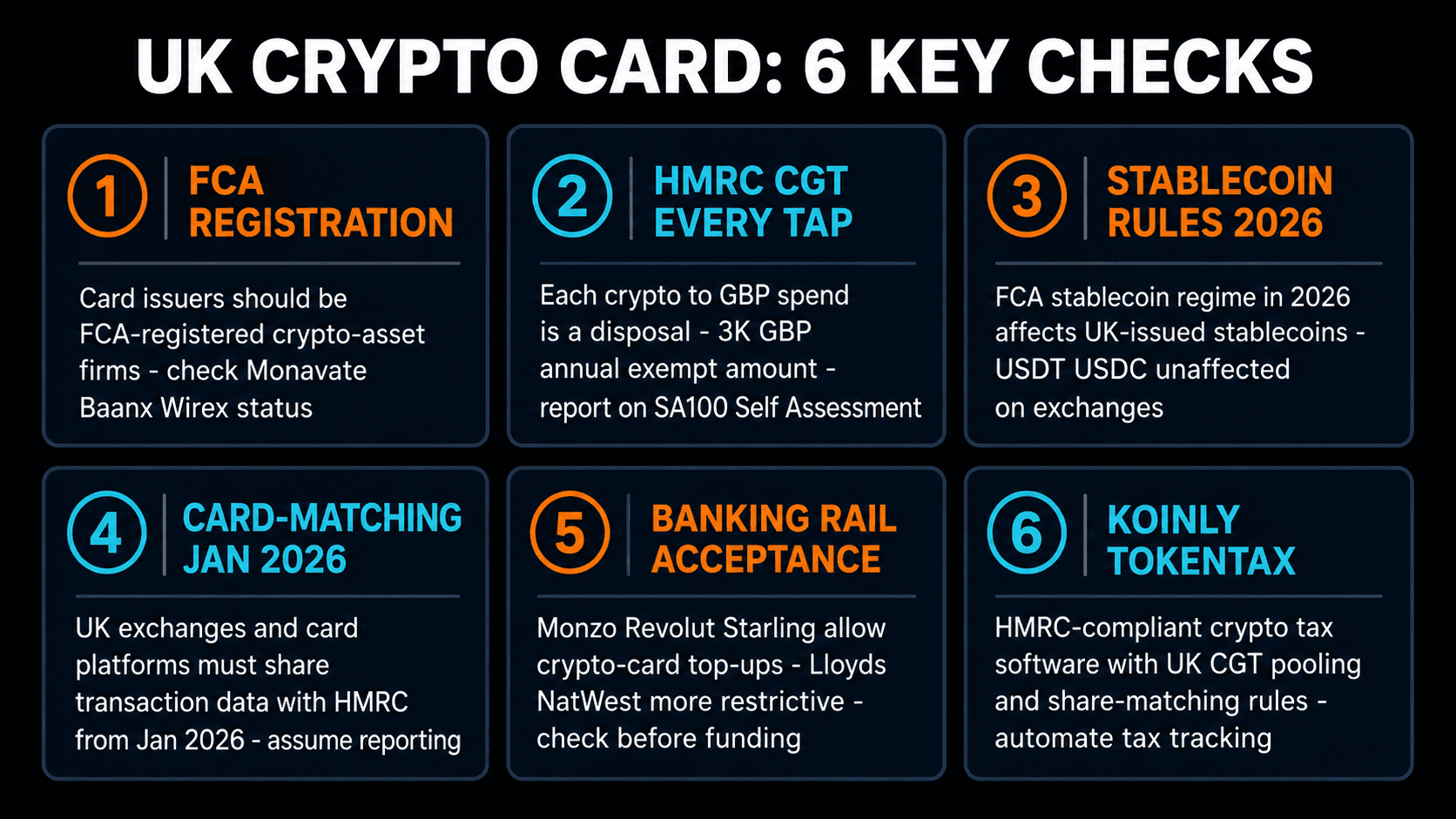

6 Things to Check Before Picking a Crypto Card in the UK

- FCA registration status. Check the FCA cryptoasset register for the card-issuing partner. Common partners and their UK firm reference numbers: Monavate (FRN 901097), Modulr, PayrNet. Cards that route through unregistered overseas EMIs may face increasing pressure to wind down UK access.

- HMRC CGT every tap. Each crypto-to-GBP spend is a disposal under TCGA 1992. Annual Exempt Amount is £3,000 for 2024-25 (down from £6,000 in 2023-24, down from £12,300 prior years). CGT rates 10%/20%. Pooling rules apply (Section 104 holding). Report on SA108.

- 2026 stablecoin rules. The FCA opened consultation on a UK stablecoin regime in March 2026. The regime will affect UK-issued stablecoins specifically. USDT/USDC access via exchanges is unaffected for the foreseeable future. UK-issued GBP stablecoins (e.g., GBPe via Monerium) operate under different rules.

- Card-matching from Jan 2026. UK exchanges and FCA-registered card platforms must share customer transaction data with HMRC. Assume any UK-issued crypto card has reported your activity. Voluntary disclosure carries lower penalties than discovery.

- Banking rail acceptance. Monzo, Revolut, and Starling broadly accept crypto-card top-ups and outbound transfers to FCA-registered exchanges. Lloyds, NatWest, and Halifax have historically been more restrictive on card platforms they perceive as "high risk". Check before linking your funding bank.

- Koinly, TokenTax, Recap. All three support HMRC pooling and share-matching rules. The 30-day same-day rule and bed-and-breakfasting rules are HMRC-specific and not handled by US-focused tools. Recap is UK-specific.

Top 5 Crypto Cards for UK Residents (2026)

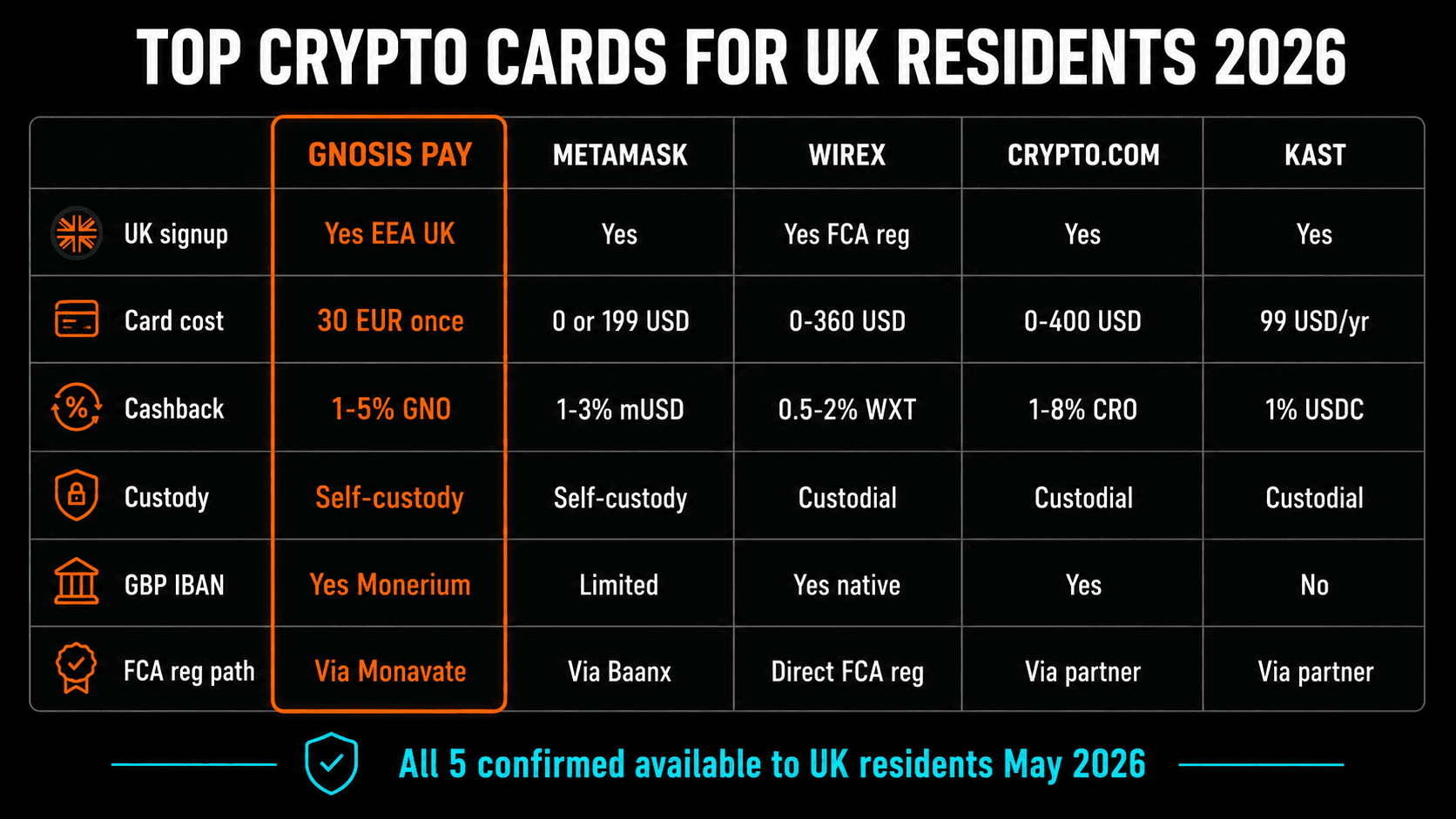

1. Gnosis Pay — Best Self-Custody Pick

Gnosis Pay is the cleanest self-custody crypto Visa in the UK. Funds stay in your Gnosis Safe smart account until tap. 30 EUR one-time card fee, zero ongoing fees, zero FX, zero off-ramp on EURe payments. Up to 5% cashback in GNO based on holdings. EUR IBAN via Monerium with SEPA Instant; GBPe support for British pound on-chain payments. Card-issuing partner Monavate is FCA-registered (FRN 901097).

- Pro: True self-custody, 0% fees, FCA-registered issuer, GBPe support

- Con: EUR-denominated card, GBP spending hits a small FX hop unless using GBPe

- Best for: UK crypto natives who want sovereignty over their funds

2. MetaMask Card — Best Mainstream Self-Custody Pick

MetaMask Card launched in the UK in February 2026. Free Virtual tier with 1% mUSD cashback. Funds stay in your MetaMask wallet on Linea, Base, Solana, or Monad. Mastercard rails. Card-issuing partner Baanx operates via Monavate (same FCA-registered EMI as Gnosis Pay). Supports EURe and GBPe natively on Linea for European/British residents wanting on-chain settlement.

- Pro: Self-custody, 9 supported tokens, GBPe on Linea, Mastercard global

- Con: Metal tier (3% cashback, zero FX) currently US-only, UK Virtual tier hits Mastercard FX rate on GBP taps

- Best for: UK Metamask users who want self-custody without changing wallets

3. Wirex Card — Best FCA-Native UK Pick

Wirex is FCA-registered directly (firm reference 928621 for Wirex Limited). Native GBP IBAN included. Multi-currency accounts for GBP/EUR/USD/AUD/CAD alongside crypto. Free Standard tier; Premium and Elite ($16.99/$31 per month) for boosted WXT cashback. The most regulatorily-clean "UK-first" option for residents who want their card issuer to be directly FCA-registered.

- Pro: Directly FCA-registered, native GBP IBAN, multi-currency accounts

- Con: Custodial, WXT cashback price-volatile, monthly fees on higher tiers

- Best for: UK residents prioritizing FCA-regulated rails

4. Crypto.com Card — Best Mature UK Option

Crypto.com Card has supported UK residents for years. Direct GBP funding via Faster Payments. Free Midnight Blue tier; higher tiers (Ruby/Royal/Obsidian) require CRO token staking (£3,500-£350,000) for 1-8% cashback. Apple Pay and Google Pay supported. Crypto.com is FCA-registered as a UK crypto-asset firm.

- Pro: Direct GBP funding (Faster Payments), mature platform, broad crypto support

- Con: Custodial, top-tier cards require sizable CRO stake-lock, fees high on Obsidian

- Best for: UK users wanting simplicity and direct GBP funding without leaving the platform

5. KAST — Best Stablecoin-First UK Pick

KAST serves UK residents with a $99/year Mastercard. 1% USDC cashback, ATM withdrawals globally, multi-chain top-up (Ethereum, Solana). 8% lifetime affiliate program if you refer friends. Smaller brand than the above but a solid mid-tier stablecoin-spend option for users who want a flat-fee card with no subscription tier mind games.

- Pro: Flat $99/year (no tier ladder), 1% USDC cashback, ATM withdrawals

- Con: Custodial, smaller brand, $99 is more than free Virtual tiers from competitors

- Best for: UK stablecoin spenders who want a fixed-cost no-surprises card

HMRC Tax Reality: What You Actually Owe

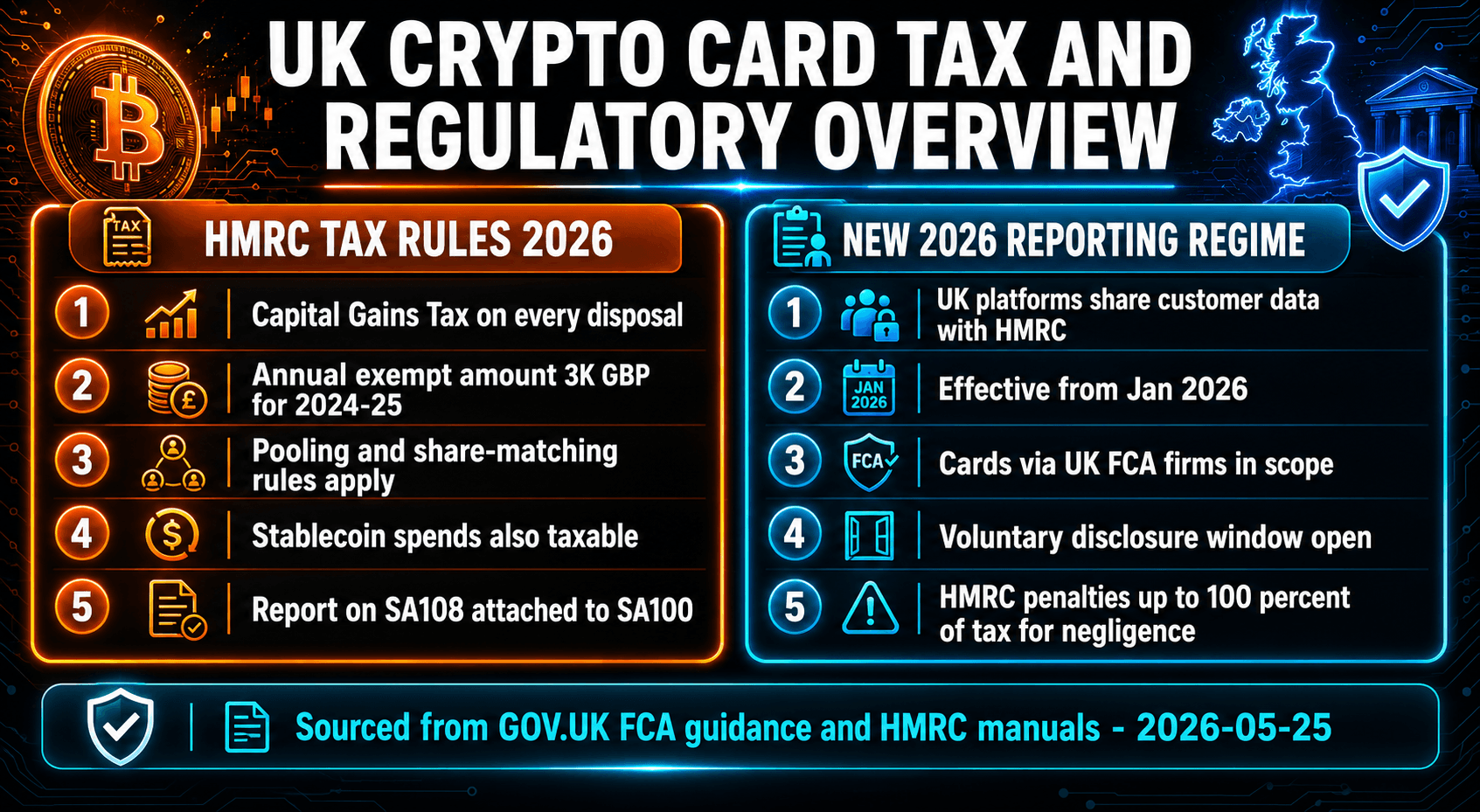

HMRC has had clear guidance since 2018: cryptocurrency is a chargeable asset for CGT purposes. Spending it is a disposal. The 2026 Cryptoasset Reporting Framework added a major teeth: UK platforms now share your transaction data with HMRC automatically.

UK residents whose crypto activity has outgrown the SA100 self-assessment route sometimes look at second-domicile planning to legally restructure their UK tax footprint — Domicillia walks through the mechanics of changing fiscal residency, Palau Digital Residency covers the digital-residency angle that some crypto-native UK earners use, and Soveraine covers the broader sovereign-wealth playbook. These are legal residency restructuring tools, not workarounds for the new 2026 HMRC reporting regime — UK obligations continue while you remain UK-resident.

- Section 104 pooling. All units of the same cryptoasset are pooled. Your ACB per unit is a weighted average across all acquisitions. When you spend, the cost-basis used is the pool average. This differs from FIFO and creates calculation complexity at scale.

- 30-day same-day rule. If you sell and rebuy the same crypto within 30 days, the rebuy is matched to the sale (not pooled). Designed to prevent "bed-and-breakfasting" tax-loss harvesting.

- Stablecoin spends still trigger small gain/loss. Driven by USD-GBP FX movement between acquisition and spend.

- Report on SA108. Capital Gains supplementary page attached to your SA100 Self Assessment. Filing deadlines: 31 October (paper) or 31 January following the tax year end (online).

- 2026 platform reporting. UK exchanges, custodians, and FCA-registered card partners must collect and share customer transaction data with HMRC. Effective January 2026.

- HMRC voluntary disclosure. If you've under-reported crypto gains historically, the Worldwide Disclosure Facility (WDF) or Contractual Disclosure Facility (CDF) routes carry materially lower penalties than discovery. Penalties for negligent non-disclosure can hit 100% of unpaid tax.

Funding Your Card from the UK

The cleanest funding path for most UK users:

- Buy USDC or USDT on an FCA-registered UK exchange. Coinbase UK, Kraken UK, Bitstamp, and Bybit (registered for UK clients) are the main options. Faster Payments (GBP) settles within minutes. Spreads typically 0.5-1.5%.

- Withdraw to the right chain. MetaMask Card: USDC on Linea or USDT on Solana. Crypto.com: USDC on Ethereum (or platform-direct). Wirex: native GBP via Faster Payments to your Wirex IBAN. Gnosis Pay: SEPA Instant in EUR or EURe direct.

- Bridge if needed. Across, Stargate, or chain-native bridges to move tokens between Ethereum/Polygon/Linea/Base.

- Bank-side checks. Monzo, Revolut, and Starling tend to be permissive of crypto on-ramp transfers. Some traditional banks flag or block transfers to crypto exchanges — if your bank does, switch the funding leg to Monzo/Revolut.

Common UK Gotchas

- Don't rely on outdated CGT allowance. The Annual Exempt Amount was cut from £12,300 (2022-23) to £6,000 (2023-24) to £3,000 (2024-25). It may be cut further. Old guides quoting higher allowances are wrong for 2026.

- HMRC's 2026 nudge letters. HMRC has sent thousands of "nudge letters" to suspected crypto investors who under-declared. Receiving one is not a formal investigation, but it's a strong signal to amend and disclose voluntarily.

- Crypto-to-crypto trades are also disposals. Swapping ETH for USDC before spending the USDC is two disposals. Many UK users miss the trade leg.

- Gifting crypto to a spouse is no-gain-no-loss. Useful for splitting CGT allowances within a household.

- Use Recap or Koinly for HMRC reports. Recap is UK-built and handles Section 104 pooling correctly. Koinly does too but the UK-specific add-ons cost extra on higher tiers.

Our Picks at a Glance

If you live in the UK and want…

- Self-custody: Gnosis Pay or MetaMask Card

- Direct FCA registration: Wirex

- Mainstream + GBP: Crypto.com

- Fixed-cost stablecoin spending: KAST

- Privacy + USDC cashback: XKard

Skip in the UK:

- Binance Card UK — paused, not currently issuing

- COCA Card — not currently UK-available

- Cards routing via non-FCA-registered overseas-only EMIs

- High-tier Crypto.com cards if you don't already hold CRO

- Any card requiring US-only physical shipping

Final Take

For most UK residents in 2026, the right move is Gnosis Pay or MetaMask Card for self-custody crypto spending and Wirex or Crypto.com Card for GBP-native funding. The 2026 HMRC reporting regime means every reasonable card you use will share your data with HMRC; pick on product fit, not on a hope of staying invisible (which is no longer possible). For most users, the self-custody plus GBP-rail combo lets you handle both crypto-native flows and everyday GBP merchant taps without compromise.

Whatever you pick: set up Recap, Koinly, or TokenTax from day one. UK users who skip tax tracking typically face significant reconciliation pain at the January Self Assessment deadline. Recap's UK-specific Section 104 pooling handling is worth the subscription if you have more than a handful of transactions per month.