Most guides about no-KYC crypto cards read like sales brochures. They talk about “financial freedom” and “privacy by default” while glossing over the part where your card gets frozen overnight and your funds disappear into a 180-day hold with zero customer support.

We’re not going to do that.

At Kardd.co, we track every major no-KYC crypto card on the market — their uptime, fee structures, card network status, and shutdown history. We recommend them when they make sense. But we also think you deserve the full picture before you load a single satoshi onto one.

Here’s the honest truth: no-KYC crypto cards are useful tools. They are not, however, risk-free. And the risks are specific, predictable, and manageable — if you know what they are.

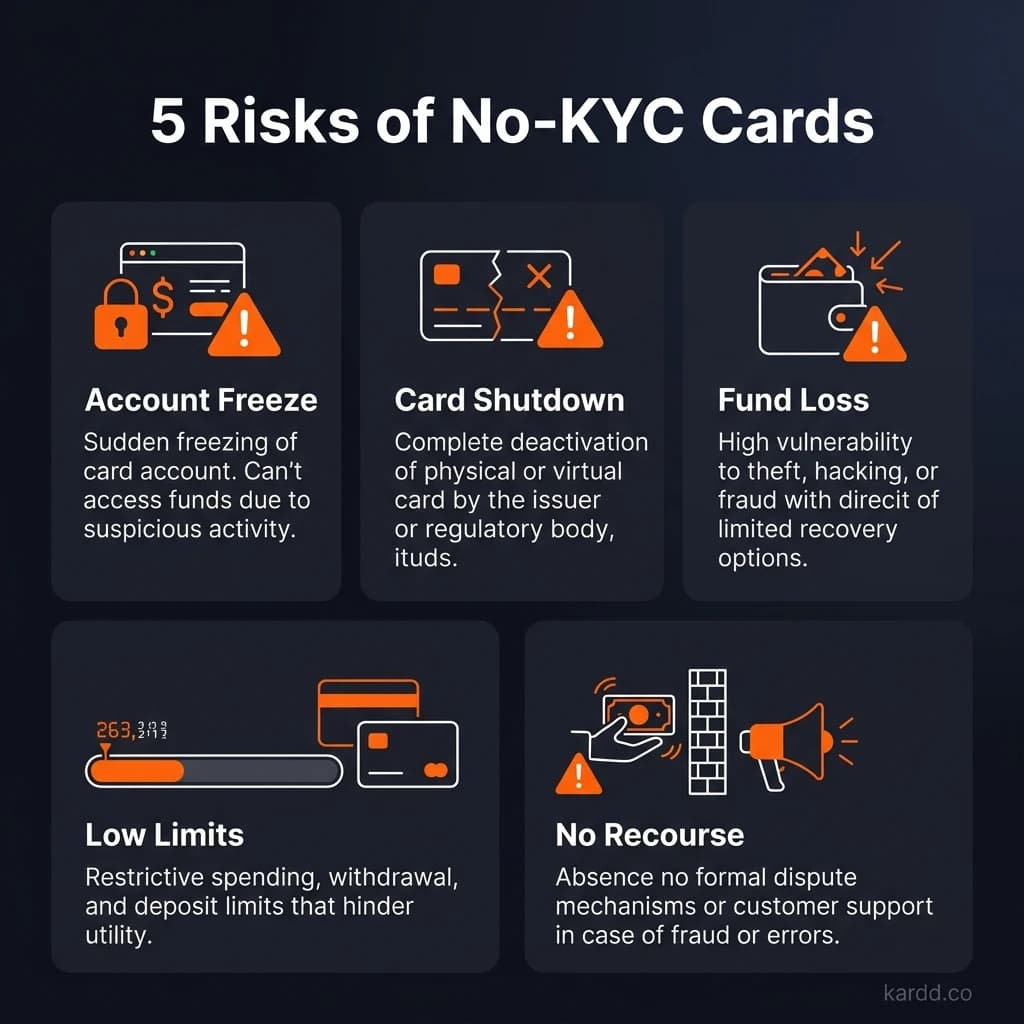

The 5 Real Risks of No-KYC Crypto Cards

Every financial product carries risk. The difference with no-KYC cards is that you have fewer safety nets when something goes wrong. Here are the five risks that actually matter.

Risk 1: Account Freezes With No Recourse

This is the most common problem users face, and the one nobody talks about.

When a no-KYC card gets flagged — whether for unusual spending patterns, a merchant dispute, or a compliance trigger from the card network — the issuer freezes the account. With a traditional bank, you call customer service, verify your identity, and get it sorted in a few days.

With a no-KYC card, you have no identity on file. There is nothing to verify. The issuer cannot unfreeze your account through standard compliance procedures because there is no KYC data to fall back on.

The result: your funds sit in a frozen state for 90 to 180 days while the issuer works through their process. Some providers return funds to the original funding source (minus fees). Others require you to complete KYC retroactively — which defeats the entire purpose.

Risk 2: Card Program Shutdowns

No-KYC card providers don’t issue Visa and Mastercard cards directly. They operate through intermediary programs — BIN sponsors, issuing partners, and payment processors that hold the actual card network license.

These intermediaries face regular audits from Visa and Mastercard. If the network decides a program carries too much risk — too many chargebacks, suspicious transaction patterns, regulatory concerns — they can terminate the program overnight.

When that happens, every card in the program stops working simultaneously. It doesn’t matter if you’ve been using yours responsibly for two years. The whole batch gets killed.

Risk 3: Operator Disappearance

The no-KYC card market has a low barrier to entry. A small team can white-label an existing card program, build a frontend, and start issuing cards within weeks.

That also means a small team can shut down the frontend, stop responding to support tickets, and disappear within days.

The operators most likely to vanish share common traits: no verifiable company registration, anonymous team members, newly launched with no track record, and aggressive referral programs designed to pull in deposits quickly.

Risk 4: Exchange Rate Manipulation and Hidden Spreads

Every no-KYC card converts your crypto to fiat when you make a purchase. The question is: at what rate?

Most providers advertise “no fees” or “low fees” while burying the real cost in the exchange rate spread. You load USDT expecting a 1:1 conversion to USD, but the actual rate applied at the point of sale is 0.985 — a hidden 1.5% fee on every transaction.

These spreads typically range from 0.5% to 1.5% on top of whatever fee the provider discloses. Some providers are transparent about this. Many are not.

How to check: Load a small amount, make a purchase, and compare the crypto debited against the fiat amount charged. If the math doesn’t match the advertised rate, you’ve found the spread.

Risk 5: Regulatory Tightening

The regulatory environment for no-KYC financial products is getting tighter, not looser.

In the EU, the Markets in Crypto-Assets (MiCA) framework is imposing new requirements on crypto service providers, including card issuers. The Travel Rule — which requires transaction data to be shared between financial institutions — is expanding to cover more crypto transactions in more jurisdictions.

The risk isn’t that no-KYC cards will disappear overnight. It’s that the program you rely on may quietly change its terms, reduce your limits, or restrict service in your region with little warning.

What Happens If Your No-KYC Card Gets Shut Down?

Understanding the shutdown process removes the panic. Here is what typically happens, step by step:

1. Notification (Day 0-3)

You receive an email or in-app notice that the card program is being discontinued. Some providers give 30 days notice. Others give 48 hours. A few give none at all — you find out when your card declines at checkout.

2. Card Deactivation (Day 1-7)

All cards in the affected program stop processing transactions. Pending transactions may or may not settle. Recurring subscriptions linked to the card will fail.

3. Fund Freeze (Day 1-90)

Remaining balances are held while the provider and their banking partner work through settlement procedures. During this period, you cannot access your funds.

4. Fund Return (Day 30-180)

Funds are returned to the original funding source — usually the crypto wallet you loaded from. The provider deducts any outstanding fees, and in some cases, a “processing fee” for the return itself.

5. Program Closure

The provider either shuts down entirely or migrates users to a new card program (often with a different BIN sponsor). If they migrate, you typically need to order a new card and may face different terms.

How to Use No-KYC Cards Safely (Practical Risk Mitigation)

None of the risks above make no-KYC cards unusable. They make them tools that require specific handling. Here’s how to protect yourself.

Never Store Large Balances

This is the single most important rule. Load only what you plan to spend in the next few days.

A no-KYC card is a spending tool, not a savings account. If the program shuts down or your account gets frozen, the amount at risk should be small enough that it doesn’t matter.

A good target: keep your card balance under $200 at any given time. Load more when you need it, not before.

Diversify Across 2-3 Providers

Don’t put all your spending capacity on a single card. Maintain active cards with at least two different providers, ideally on different card networks (one Visa, one Mastercard).

If one program goes down, you still have a backup. This also lets you compare actual exchange rates and fee structures between providers.

Use Established Providers Tracked on Kardd.co

This is where due diligence matters most. Providers with a longer track record, transparent fee structures, and consistent uptime are measurably safer than new entrants.

Kardd.co tracks provider status, uptime history, and user-reported issues across every major no-KYC card. We update this data weekly. Before loading funds onto any card, check its current status on our directory.

Check Card Status Weekly Before Loading

Card programs can change status quickly. Before you load funds, take 30 seconds to verify:

- Is the provider’s website operational?

- Are there recent user reports of issues?

- Has Kardd.co flagged any status changes?

Start With Small Test Transactions

When trying a new provider, start with the minimum load amount. Make a small purchase — an online subscription or a coffee. Verify that the transaction processes, the exchange rate matches what’s advertised, and the deducted amount is correct.

Keep Records of Your Funding Transactions

Save screenshots or records of every time you load funds onto a no-KYC card. Keep the transaction hash from the blockchain, the amount loaded, and the date.

If a provider shuts down and you need to dispute or recover funds, these records are your only proof of what you’re owed. Without KYC, the provider has no account history tied to your identity — your transaction records are your paper trail.

Which No-KYC Cards Are Most Reliable?

Reliability in this market comes down to three factors: how long the provider has been operating, how transparent their fee structure is, and whether they’ve survived at least one card network audit cycle.

XKard — The Most Established No-KYC Option

XKard has the longest consistent track record among no-KYC crypto card providers currently operating. They offer both Visa and Mastercard options with zero KYC requirements, and they’ve maintained uninterrupted service through multiple periods where other providers went offline.

What sets XKard apart is operational stability. In a market where providers routinely appear and disappear, XKard has been consistently available with transparent fee structures and responsive support channels.

Other Established Options

BingCard — Another long-running provider with a solid track record. Known for competitive exchange rates and a straightforward loading process.

KAST — Offers both virtual and physical card options with no KYC. Has maintained consistent availability and transparent pricing.

How Kardd.co Rates Reliability

We don’t just list cards — we rate them. Every provider on Kardd.co is assigned a tier based on our assessment of their operational reliability:

- Gold Tier — Longest track record, survived multiple audit cycles, transparent operations, consistent uptime. Lowest risk among no-KYC options.

- Silver Tier — Established provider with good track record but shorter history or less transparency in some areas. Moderate risk.

- Bronze Tier — Newer provider or one with limited track record. Higher risk — use with smaller balances and more caution.

These tiers are updated regularly based on ongoing monitoring. Check the best no-KYC crypto cards for 2026 for the full ranked directory.

No-KYC Card Safety vs KYC Card Safety

Understanding the tradeoff clearly helps you make a better decision. Here’s how the two approaches compare on the dimensions that actually matter.

| Factor | No-KYC Crypto Card | KYC Crypto Card |

|---|---|---|

| Privacy | High — no personal data required | Low — full identity verification |

| Account Recovery | Difficult — no identity to verify | Standard — identity-based recovery |

| Freeze Resolution | Slow (90-180 days), limited recourse | Faster (days to weeks), regulated process |

| Regulatory Risk | Higher — may face restrictions | Lower — already compliant |

| Provider Stability | Variable — less regulated operators | Higher — regulated entities |

| Chargeback Protection | Minimal to none | Standard consumer protections |

| Fee Transparency | Variable — hidden spreads common | Generally more transparent |

| Spending Limits | Typically lower ($500-$10,000/month) | Higher with full KYC |

| Setup Speed | Minutes — no verification wait | Hours to days for KYC approval |

| Surveillance Exposure | Minimal | Full transaction monitoring |

The honest takeaway: KYC cards are objectively safer in terms of consumer protection and account recovery. No-KYC cards are objectively better for financial privacy. You’re trading one form of safety for another.

For a deeper comparison, see our full breakdown: No-KYC vs KYC Crypto Cards — What’s the Real Difference?

FAQ

Can I get my money back if a no-KYC card shuts down?

In most cases, yes — but not quickly. When a card program shuts down, providers typically return remaining balances to the original funding source (the crypto wallet you loaded from). This process takes anywhere from 30 to 180 days. Some providers deduct a processing fee from the returned amount. However, if the operator disappears entirely — which is rare with established providers but does happen with newer ones — recovery becomes significantly harder. This is why keeping balances low and using providers tracked on Kardd.co matters.

Are no-KYC crypto cards legal?

In most jurisdictions, using a no-KYC crypto card is not illegal for the cardholder. The legal burden falls on the provider to comply with applicable regulations. However, the legality varies by country and is changing rapidly. The EU’s MiCA framework and expanding Travel Rule requirements are pushing more providers toward mandatory KYC. Using a no-KYC card to evade tax obligations or launder money is illegal everywhere. For legitimate privacy-focused spending, no-KYC cards currently operate in a legal gray area in most countries.

Which no-KYC crypto card is the safest?

No no-KYC card offers the same safety guarantees as a regulated bank product. That said, XKard has the strongest track record among currently operating no-KYC providers based on uptime, fee transparency, and longevity. BingCard and KAST are also established options. The safest approach is to diversify across multiple providers, keep balances low, and check Kardd.co for current status before loading funds.

Can funds on a no-KYC card be seized?

Yes. No-KYC does not mean untouchable. If a card program is shut down due to a regulatory action, law enforcement investigation, or card network compliance order, all funds on all cards in that program can be frozen. The “no-KYC” aspect means the provider doesn’t have your identity — but the funds are still held by a regulated financial intermediary somewhere in the chain. Seizure is uncommon for individual users but absolutely possible at the program level.

The Bottom Line

No-KYC crypto cards are a legitimate tool for privacy-conscious spending. They let you use cryptocurrency in the real world without handing over your passport, and for many users, that tradeoff is worth it.

But they are not safe in the way a regulated bank account is safe. They carry specific, real risks — account freezes with slow resolution, program shutdowns, hidden fees, and an evolving regulatory landscape that may restrict them further.

The users who have the best experience with no-KYC cards are the ones who treat them like what they are: a spending tool with a limited trust window. Load small amounts. Diversify providers. Check status before loading. Keep records.

If you follow those principles, no-KYC cards are a practical and useful part of a privacy-focused financial setup. For broader operational security guidance, tools like Undetectr can help you stay ahead of detection and tracking across the web.

Looking for specific card recommendations? Check our best no-KYC crypto cards for 2026 or learn how to use a no-KYC crypto card with Apple Pay.

Cards Mentioned in This Guide

This article is for informational purposes only and does not constitute financial advice. Cryptocurrency products carry inherent risk. Always do your own research before using any financial product. Full affiliate disclosure