Tria Card Review 2026: Self-Custodial Visa, Up to 6% Cashback, 150+ Countries

Our verdict: Tria is a self-custodial Visa card wrapped inside a neobank app — you hold the keys via TSS while spending in 150+ countries. Pros: genuine self-custody, up to 6% cashback, zero FX and zero monthly fees, 1,000+ tokens across 200+ chains, up to 12% APY on idle stablecoins, and a lighter KYC flow (no proof of address). Cons: the 6% headline is a promotional ceiling not a flat rate, the higher rate often hinges on an access code, and card issuance costs ~$20-$90. A strong pick if you want to spend crypto without handing custody to an exchange.

Tria is one of the few crypto cards in 2026 that lets you spend from a wallet you actually control. Most cards in this category — KAST, Kolo, Crypto.com, Bybit — are custodial: you top up a balance the provider holds. Tria takes the opposite approach, using a threshold-signature (TSS) self-custodial wallet so your assets stay yours until the instant a Visa authorization pulls from them.

We tested the proposition against Tria's official site, its whitepaper, the App Store and Google Play listings, and third-party trackers. The product is real, shipped, and reports 500K+ users. What follows is the honest breakdown of where Tria wins and where the marketing runs ahead of the guarantee.

Key Features

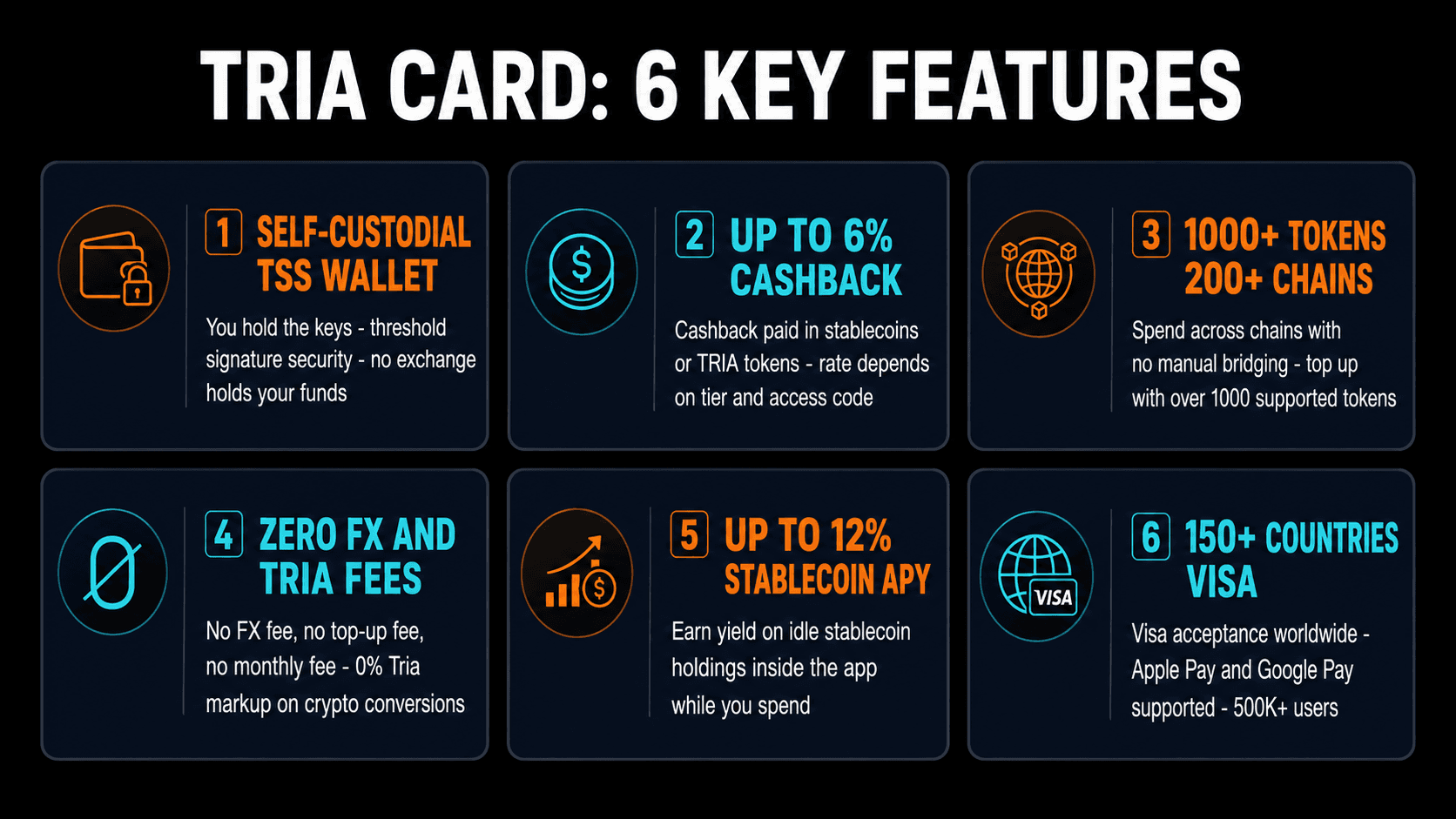

- Self-custodial TSS wallet. Tria splits your signing key using threshold-signature cryptography, so neither Tria nor any single party can move your funds alone. You keep custody of the spending balance — the structural opposite of an exchange card.

- Up to 6% cashback. Paid in stablecoins (USDC) or TRIA tokens. The 6% figure is a promotional ceiling, frequently tied to applying an access code at signup. Verify the live rate in-app before treating it as guaranteed.

- 1,000+ tokens across 200+ chains. Top up from a huge range of assets with no manual bridging — Tria abstracts the cross-chain routing so you spend without thinking about which network a token sits on.

- Zero FX, zero monthly, zero top-up fees. Tria lists a 0% in-house markup on crypto conversions, no monthly subscription, no top-up fee, and no decline fee. That fee profile is genuinely competitive.

- Up to 12% APY on stablecoins. Idle stablecoin holdings inside the app can earn yield while you spend, turning the card account into a light savings layer.

- $1,000,000 daily spend limit. Monthly spend and ATM withdrawals are listed as unlimited — high ceilings relative to most prepaid crypto cards.

- 150+ countries on Visa. Apple Pay and Google Pay supported. Both virtual and physical card formats are available.

- Lighter KYC. Email, phone, and government ID required; proof of address and selfie listed as not required. It is not a no-KYC card, but the documentation burden is lower than fully verified alternatives.

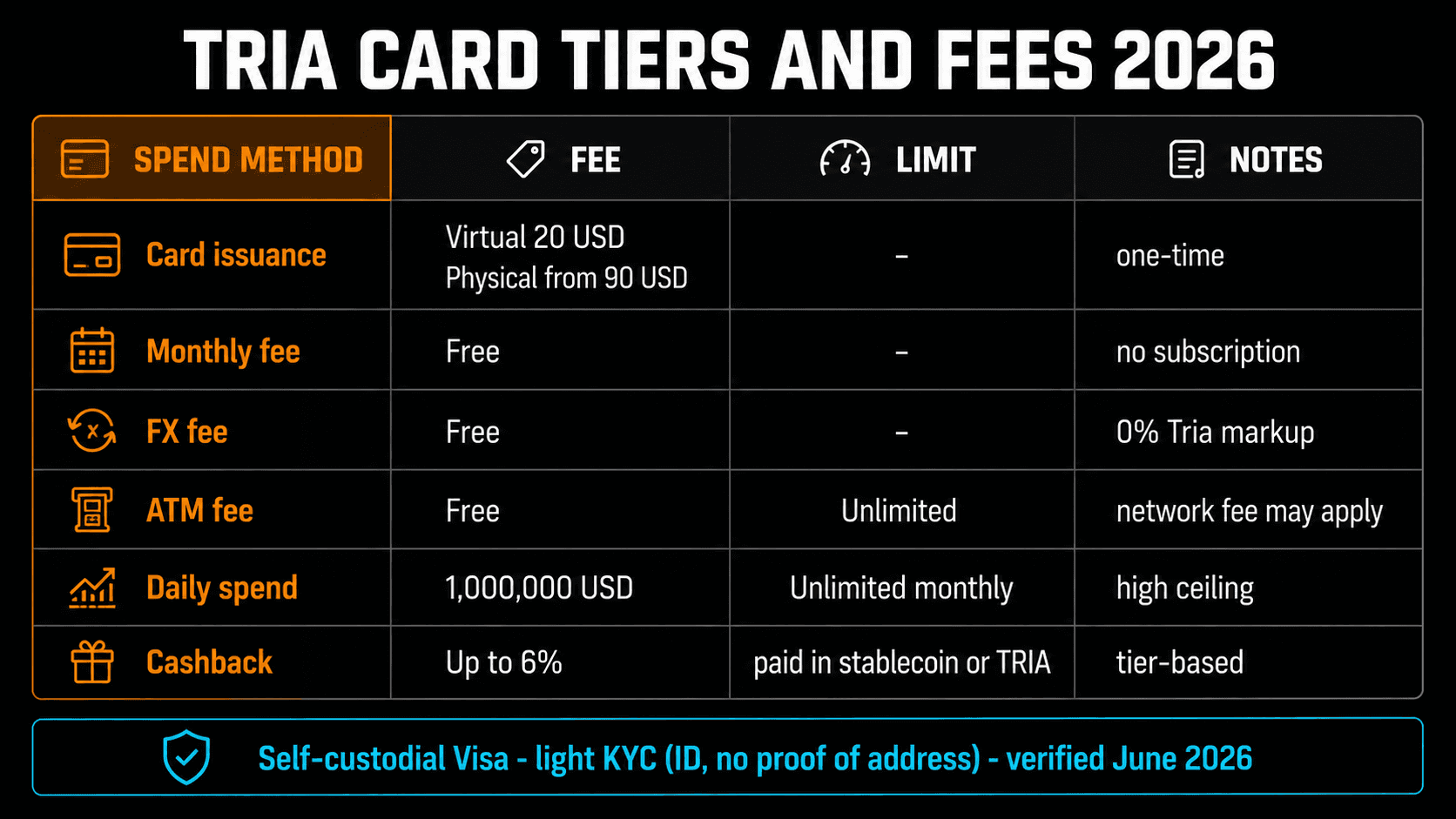

Pricing & Tiers

| Item | Cost | Notes |

|---|---|---|

| Virtual card | ~$20 issuance | Apple Pay / Google Pay ready |

| Physical (Signature) | ~$90 issuance | One-time, metal-tier styling |

| Monthly fee | Free | No subscription |

| FX fee | Free | 0% Tria markup |

| ATM fee | Free (Tria side) | Operator fee may apply |

| Cashback | Up to 6% | Stablecoin or TRIA, tier-based |

The economics are unusually clean for a self-custody card. The recurring costs — FX, monthly, top-up — are the line items that quietly erode value on most crypto cards, and Tria zeroes them out. Your real cost is the one-time issuance fee, plus whatever conversion spread the underlying market applies when you fund from a volatile token rather than a stablecoin.

How the Tria Card Works

Tria positions itself as a self-custodial neobank rather than a card with a wallet bolted on. Funds sit in your TSS wallet across whichever chains you hold them on. When you tap, Tria's routing converts the needed amount at spend time and settles the Visa transaction. Because the conversion happens at the point of sale, spending volatile assets exposes you to short-term price moves — funding from USDC or another stablecoin removes that risk and is the cleanest way to use the card day to day.

One important honesty note: a self-custodial card still touches a regulated payment rail, so a government ID is required and your transactions are processed by Visa and Tria's issuing partners. Self-custody here means you control the asset until spend — it does not mean the card is anonymous. If anonymity is your goal, read our guide on whether no-KYC crypto cards are safe.

Pros & Cons

Pros

- Genuine self-custody via TSS wallet

- Up to 6% cashback (stablecoin or TRIA)

- Zero FX, zero monthly, zero top-up fees

- 1,000+ tokens across 200+ chains, no manual bridging

- Up to 12% APY on idle stablecoins

- 150+ countries, Apple Pay + Google Pay

- Lighter KYC (no proof of address / selfie)

- High $1M daily spend ceiling

Cons

- 6% is a promotional ceiling, not a flat rate

- Top rate often hinges on an access code

- Card issuance fee (~$20-$90)

- Not a no-KYC card — ID required

- Point-of-sale conversion risk on volatile assets

- TRIA-denominated cashback carries token risk

- Newer brand vs established exchange cards

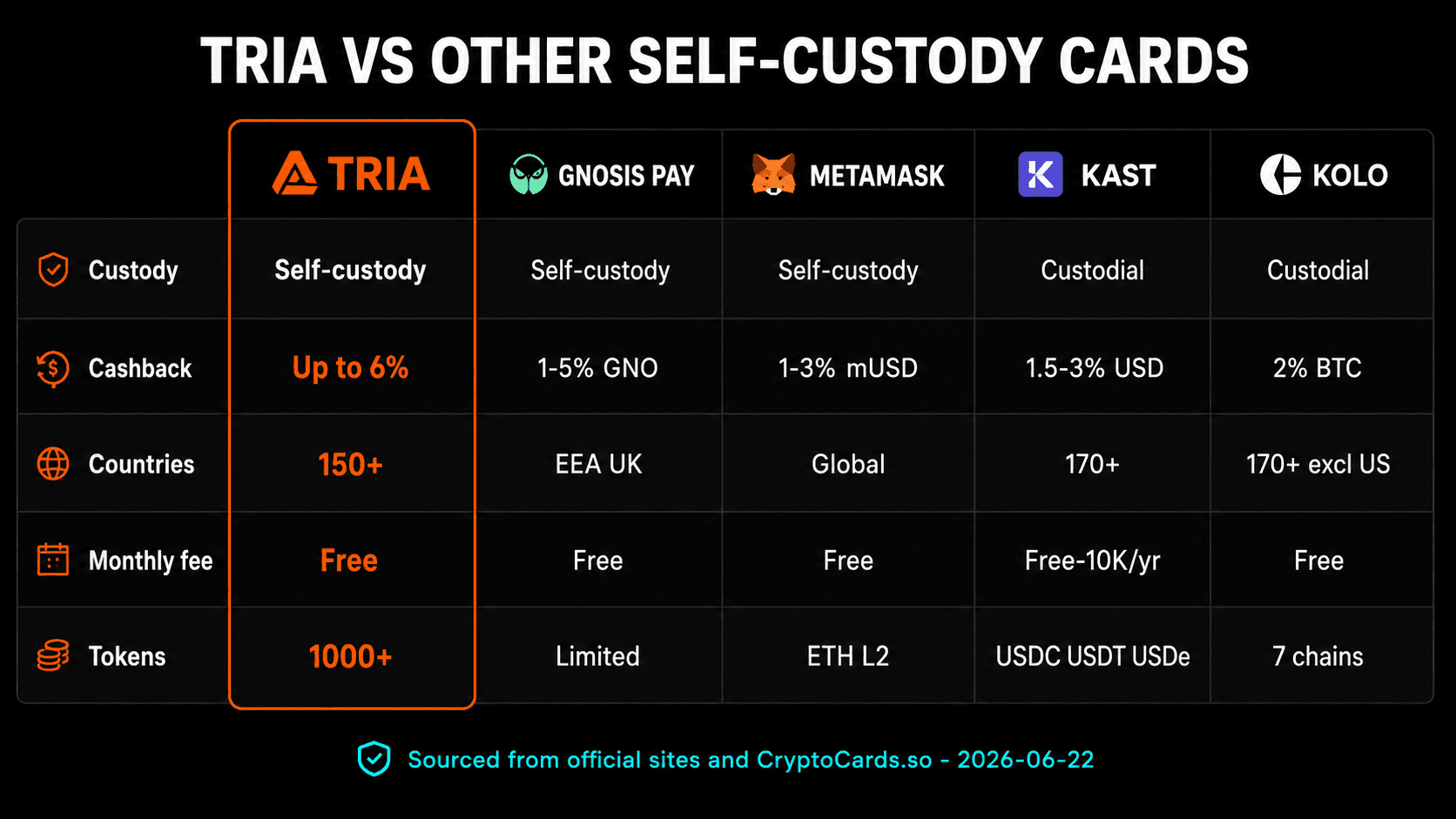

Tria vs Other Self-Custody Cards

| Card | Custody | Cashback | Countries |

|---|---|---|---|

| Tria | Self-custody | Up to 6% | 150+ |

| Gnosis Pay | Self-custody | 1-5% GNO | EEA/UK |

| MetaMask | Self-custody | 1-3% mUSD | Global |

| KAST | Custodial | 1.5-3% USD | 170+ |

| Kolo | Custodial | 2% BTC | 170+ (excl US) |

Who Should Get the Tria Card

Get Tria if: self-custody is a hard requirement and you still want a card that spends in 150+ countries. The fee profile (zero FX, zero monthly) rewards frequent and cross-border spenders, and the multi-chain support means you are not forced to consolidate onto one network before funding. If you already keep assets across several chains and want to spend without first off-ramping to an exchange, Tria is one of the cleanest options in 2026.

Skip Tria if: you want a guaranteed flat cashback rate with no asterisks (the 6% is promotional), or you want a fully custodial set-and-forget card with a longer track record — in which case KAST or Crypto.com are more established. Skip it if you specifically need a no-KYC card — Tria requires ID.

Final Verdict: 84% Kardd Score

Tria scores 84% in our independent rating. It earns the high mark by delivering something most of the category does not — real self-custody — without sacrificing global Visa acceptance or stacking on the FX and monthly fees that quietly drain value elsewhere. The points it loses are for the promotional nature of the 6% headline, the access-code dependency on the top rate, and a shorter track record than the incumbent exchange cards.

For privacy-minded, multi-chain spenders who refuse to hand custody to an exchange, Tria is close to the top of the self-custody field alongside Gnosis Pay and MetaMask Card.