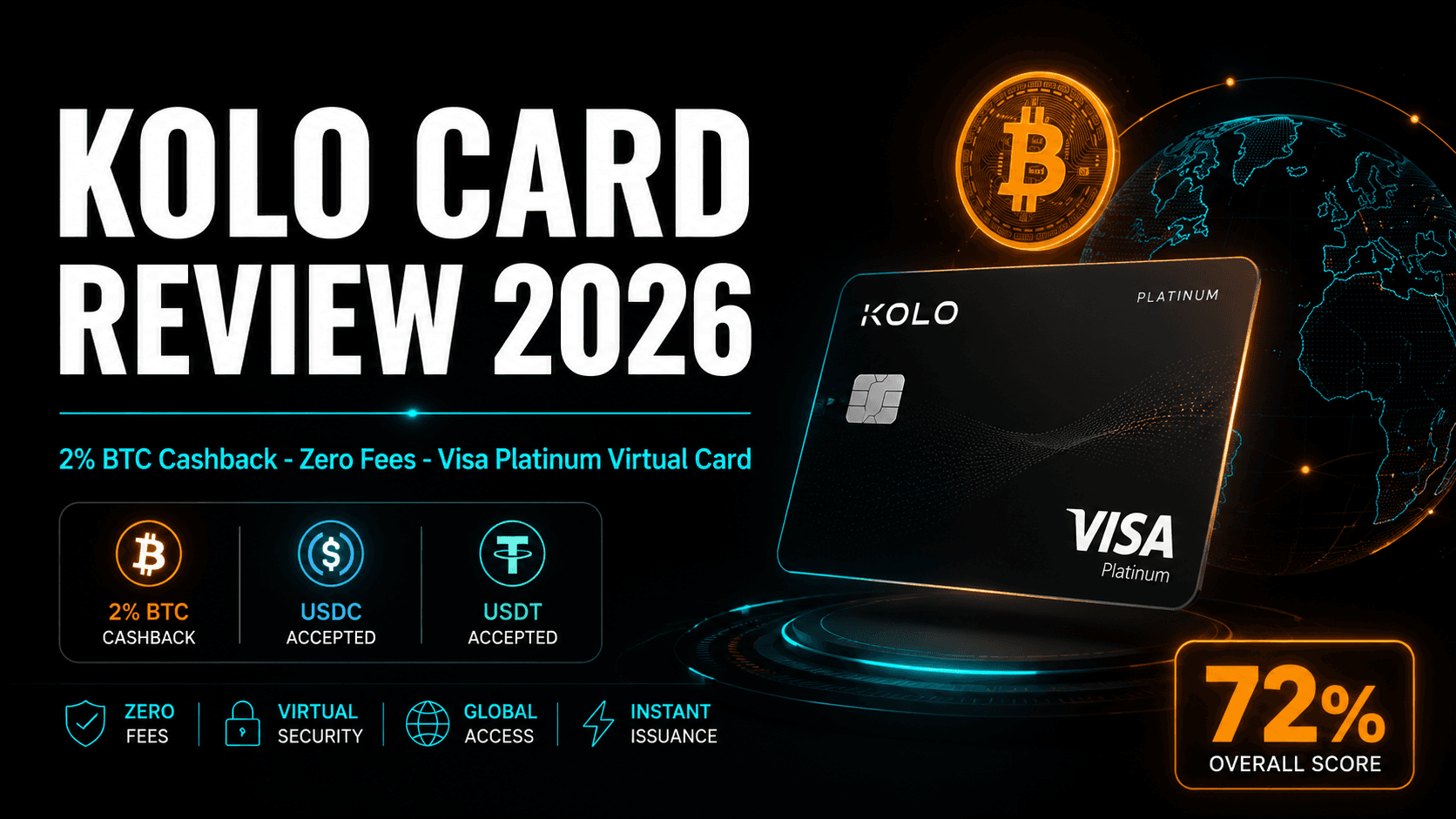

Kolo Card Review 2026: 2% BTC Cashback, Zero-Fee Visa Platinum Virtual Card

Our verdict: Kolo is a zero-fee, custodial Visa Platinum virtual card that pays 2% cashback in Bitcoin and shines for stablecoin spenders. Pros: no annual/monthly/inactivity fees, 0% FX markup on USDT/USDC/EURC, 170+ countries, direct SEPA send to EU banks, MiCA-ready. Cons: cashback was quietly cut from 5% to 2%, the rate is changeable at Kolo's discretion, it's custodial (Kolo holds your funds), virtual-only with limited ATM access, and not available in the US. A solid stablecoin remittance card, not a Bitcoin-accumulation play anymore.

Kolo's story changed in 2026, and any honest review has to start there. The card built its reputation on a headline 5% Bitcoin cashback rate. The current public homepage now markets 2% BTC cashback, and Kolo's own Terms of Use (v2.1, 31 December 2025) make clear the reward program can be modified, suspended, or terminated at any time at Kolo's sole discretion. If you arrived here chasing the old 5% number, recalibrate: the live figure is 2%.

That said, Kolo still has a real place in the market — just a different one. Its strongest claim was never really the cashback. It is the zero-fee structure and the 0% FX markup on stablecoin spending, which make it one of the cheapest cards to run if you spend USDC, USDT, or EURC. We verified the specs against Kolo's official site, its Terms, and CoinDesk's launch coverage.

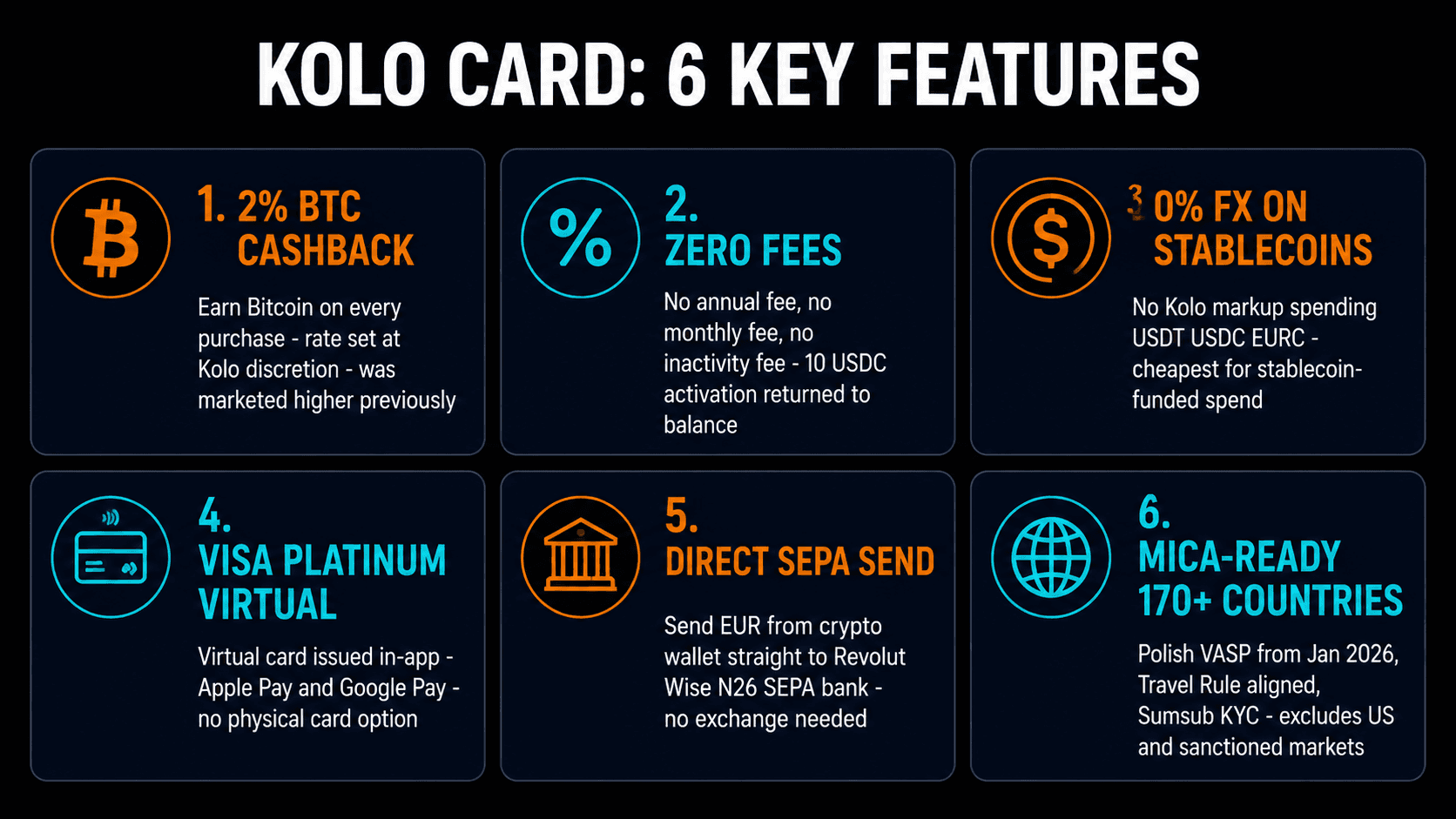

Key Features

- 2% BTC cashback. Paid in Bitcoin on every purchase. The rate is set at Kolo's discretion and was previously marketed at 5%, so treat 2% as the live headline rather than a fixed promise.

- Zero fees. No annual fee, no monthly fee, no inactivity fee. The 10 USDC activation charge is returned to your balance, so the net activation cost is zero.

- 0% FX markup on stablecoins. Spending USDT, USDC, or EURC carries no Kolo markup — the single best reason to use the card. Non-USD purchases still incur the Visa network FX rate.

- Visa Platinum virtual card. Issued in-app, ready for Apple Pay and Google Pay. There is no physical card and ATM access is limited.

- Direct SEPA send. Move EUR from your Kolo wallet straight to Revolut, Wise, N26, or any SEPA bank account without routing through a separate exchange — genuinely useful for EEA users and euro-corridor remittances.

- 7 supported networks. Ethereum, BNB Chain, Arbitrum, Base, Solana, Stellar, and Polygon.

- 170+ countries, MiCA-ready. Travel Rule aligned with Sumsub KYC. Crypto-asset services moved to a Polish VASP (BURVIX) from January 2026. Excludes the US and sanctioned markets.

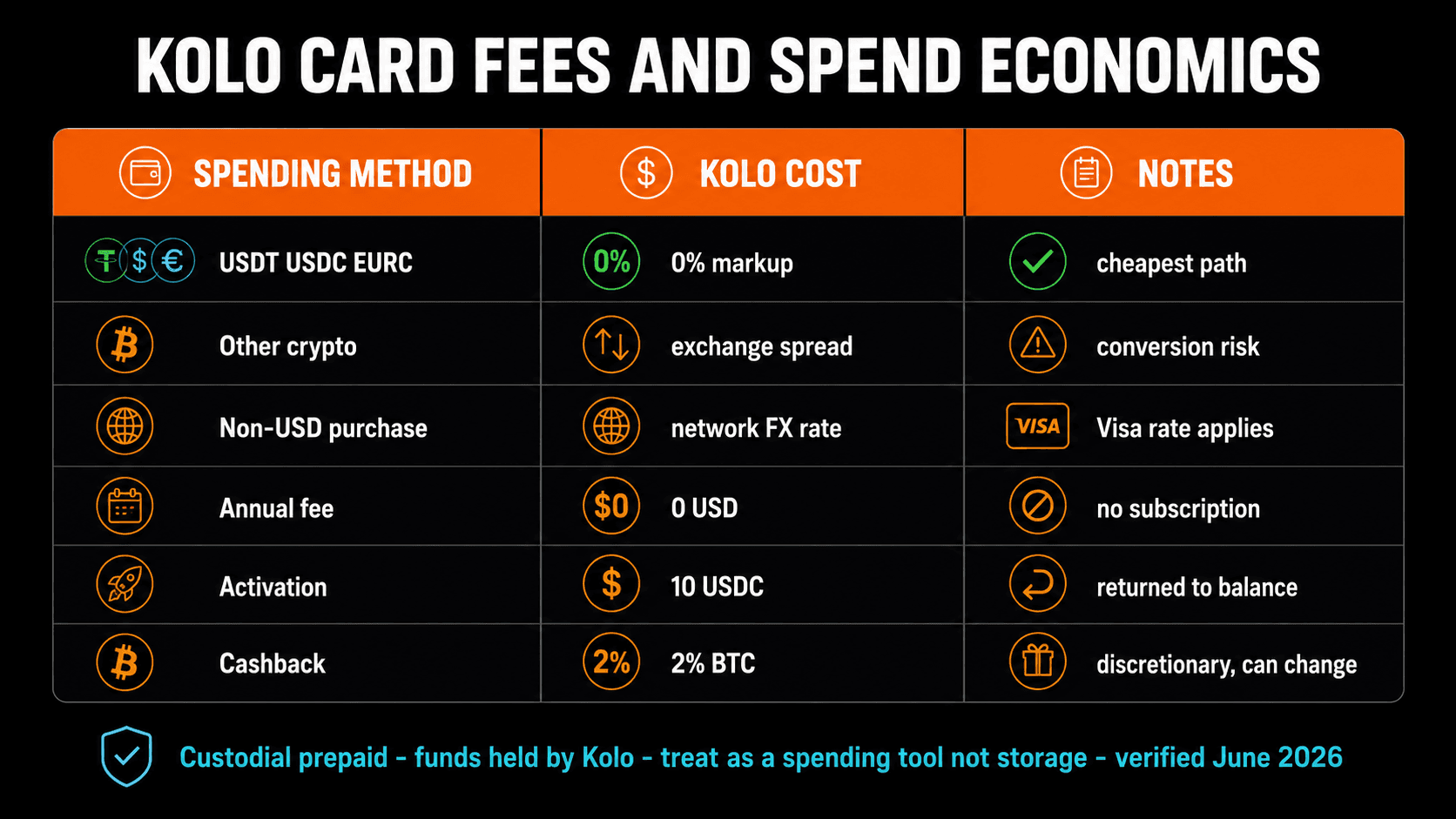

Fees & Spend Economics

| Spending method | Kolo cost | Notes |

|---|---|---|

| USDT / USDC / EURC | 0% markup | Cheapest path |

| Other crypto | Exchange spread | Conversion risk |

| Non-USD purchase | Network FX rate | Visa rate applies |

| Annual fee | $0 | No subscription |

| Activation | 10 USDC | Returned to balance |

| Cashback | 2% BTC | Discretionary, can change |

If you spend from stablecoins, Kolo is structurally cheaper than many prepaid competitors that stack a conversion spread on top of FX. That is the durable reason to hold it. The 2% BTC cashback is a nice extra, not the headline anymore — several free cards now match or beat it, so Kolo's "biggest BTC cashback" slogan is marketing positioning rather than an independent benchmark.

Pros & Cons

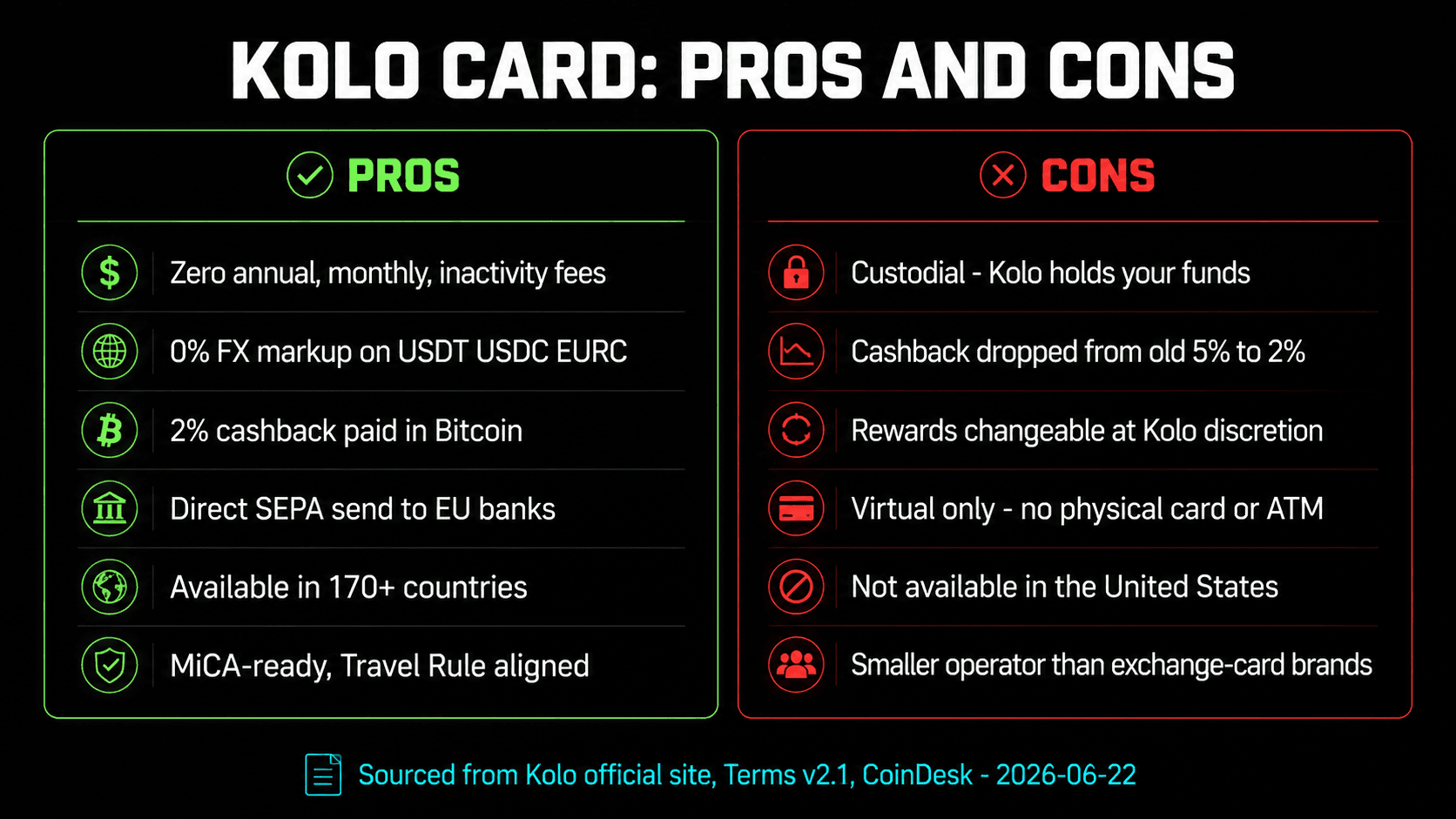

Pros

- Zero annual, monthly, inactivity fees

- 0% FX markup on USDT/USDC/EURC

- 2% cashback paid in Bitcoin

- Direct SEPA send to EU banks

- 170+ countries, 7 networks

- MiCA-ready, Travel Rule aligned

- Activation fee fully refunded

Cons

- Custodial — Kolo holds your funds

- Cashback cut from 5% to 2%

- Rewards changeable at Kolo's discretion

- Virtual-only — no physical card

- Limited ATM access

- Not available in the US

- Smaller operator than exchange-card brands

Kolo Card vs Competitors

| Card | Cashback | Custody | US? |

|---|---|---|---|

| Kolo | 2% BTC | Custodial | No |

| KAST | 1.5-3% USD | Custodial | Limited |

| Bleap | Up to 3% | Self-custody | No |

| Tria | Up to 6% | Self-custody | Varies |

| Crypto.com | 1-8% CRO | Custodial | Yes |

Who Should Get the Kolo Card

Get Kolo if: you live outside the US, you mostly spend stablecoins, and you want a genuinely zero-fee card with a little Bitcoin cashback on top. The 0% FX markup and direct SEPA send make it a strong fit for EEA users and euro-corridor remittances, where the ability to push EUR straight to a bank account without an exchange hop has real, recurring value.

Skip Kolo if: you want self-custody (look at Tria or Gnosis Pay), you need a physical card or reliable ATM access, you live in the US, or you were relying on the old 5% cashback that no longer reflects the live product. For pure Bitcoin accumulation, the 2% rate is no longer category-leading.

Final Verdict: 72% Kardd Score

Kolo scores 72%. The zero-fee structure and 0% stablecoin FX are genuinely good and keep the card relevant. The score is held back by the cashback downgrade, the discretion Kolo reserves over its reward rules, the custodial model, virtual-only format, and US exclusion. Treat Kolo as a low-cost stablecoin spending and remittance tool — not a long-term storage venue and not the BTC-stacking machine it was once marketed as.