Crypto Debit Cards With No Foreign Transaction Fees 2026: 7 Tested

Quick answer: Traditional bank debit cards charge 2.5–3.5% foreign transaction fees. The best crypto debit cards charge 0%. At $15K/year of international spending that's $450–$525 saved before you even count cashback. Top picks tested in 2026: Gnosis Pay Card (0% FX, self-custody, up to 5% GNO cashback, EEA/UK), Coinbase Card (0% FX, US prepaid Visa, 4% cashback), and MetaMask Metal (0% FX in 48 countries, $199/yr, 3% cashback on first $10K). Watch the gotchas: BTC funding adds 0.5–1.5% conversion at swipe, and the Dynamic Currency Conversion prompt at terminals can wipe out your savings if you accept it.

A $1,000 week in Tokyo costs about $30 in foreign transaction fees on a regular bank card. On a 0% FX crypto card it costs $0. Over a year of international spending that is $300–$900 staying in your pocket instead of disappearing into your bank's margin. For digital nomads and frequent travelers spending $30K+ per year abroad, the swing is over $1,000 per year before you even count cashback.

But the "0% FX" line on a marketing page is not the same as 0% total cost. Some cards charge 0% FX markup and then hit you with a 1.7% crypto-to-fiat conversion fee when you fund from BTC. Others advertise 0% FX while using an exchange rate spread that quietly costs an extra 0.3–0.5% per transaction. This guide tests 7 crypto cards with genuine 0% issuer FX, shows you the real total cost at three spending levels, and flags the gotchas that wipe out your savings.

Why Foreign Transaction Fees Matter More Than You Think

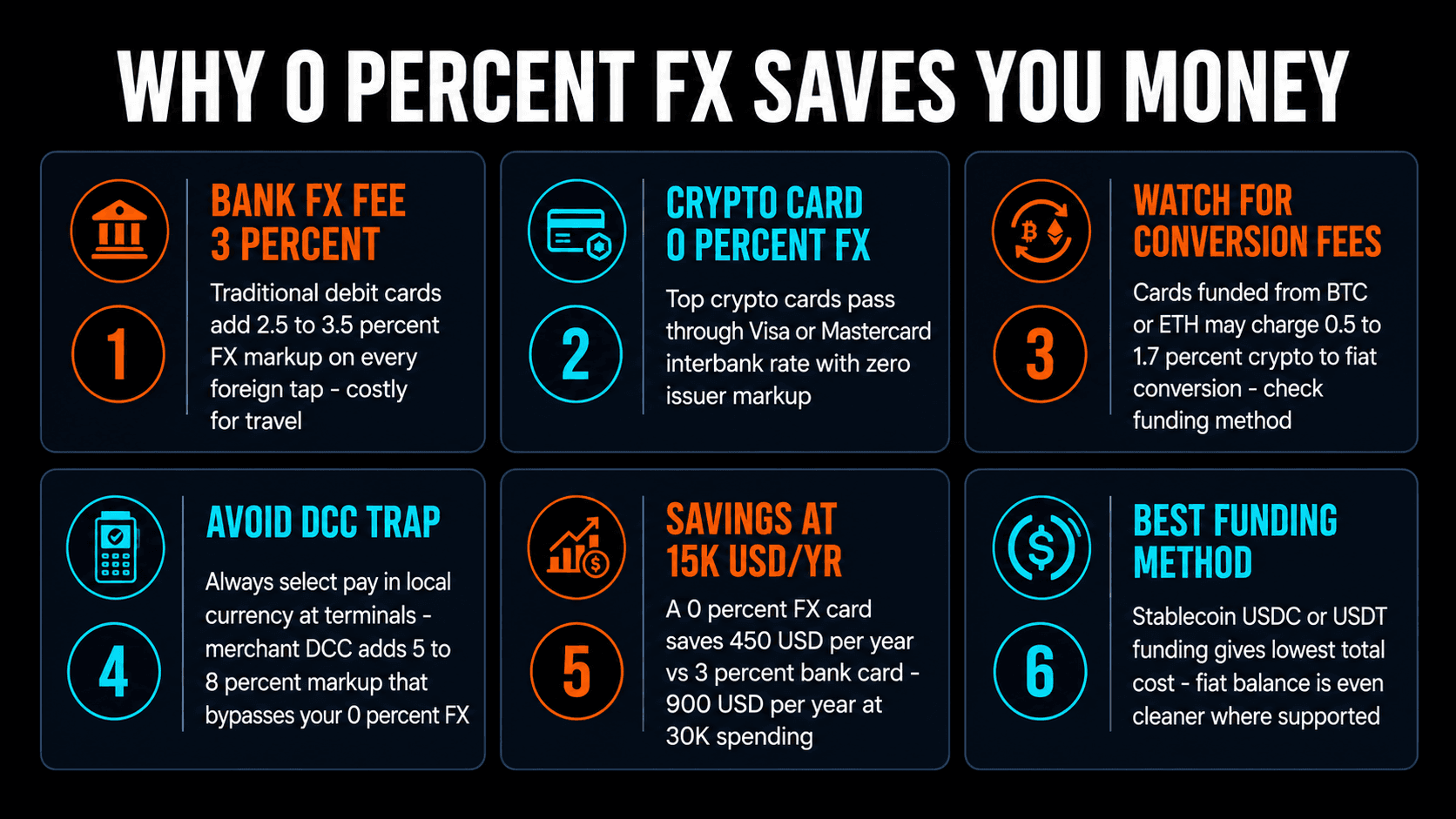

When you spend $1,000 in a foreign currency on a traditional bank card, three costs typically stack on top of the headline transaction:

- FX markup (2.5–3.5%). The bank adds a percentage on top of the Visa or Mastercard interbank rate. Cost on $1,000: $25–$35.

- Exchange rate spread. The bank uses a rate slightly worse than the mid-market rate. Cost on $1,000: $2–$5.

- Crypto-to-fiat conversion (crypto cards only). If your card funds from BTC or ETH, the card converts crypto to fiat at point of sale. Cost: 0–1.7%.

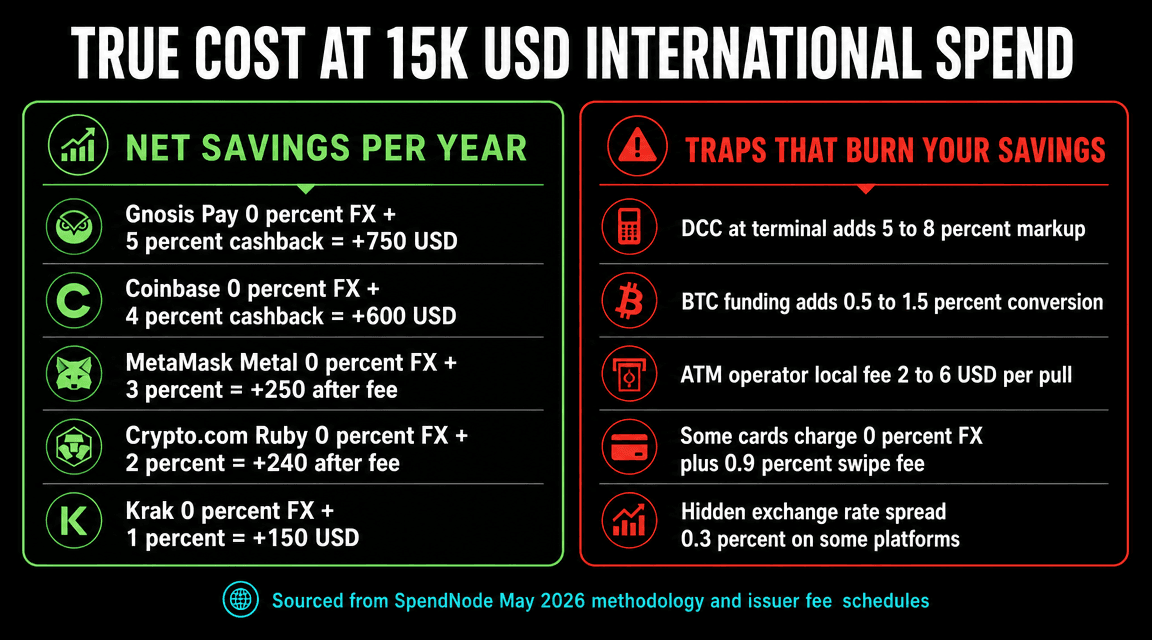

A 0% FX crypto card eliminates layer 1 entirely. Layer 2 is the same on every card that uses the Visa/Mastercard network. Layer 3 only exists on crypto cards and can be reduced or eliminated by funding the card with stablecoins (USDC, USDT, EURC) or fiat balance instead of volatile crypto. Total real savings at $15,000 per year of international spending: $450–$525 versus a 3% bank card, before cashback is counted.

Top 5 Crypto Cards With 0% Foreign Transaction Fees (2026)

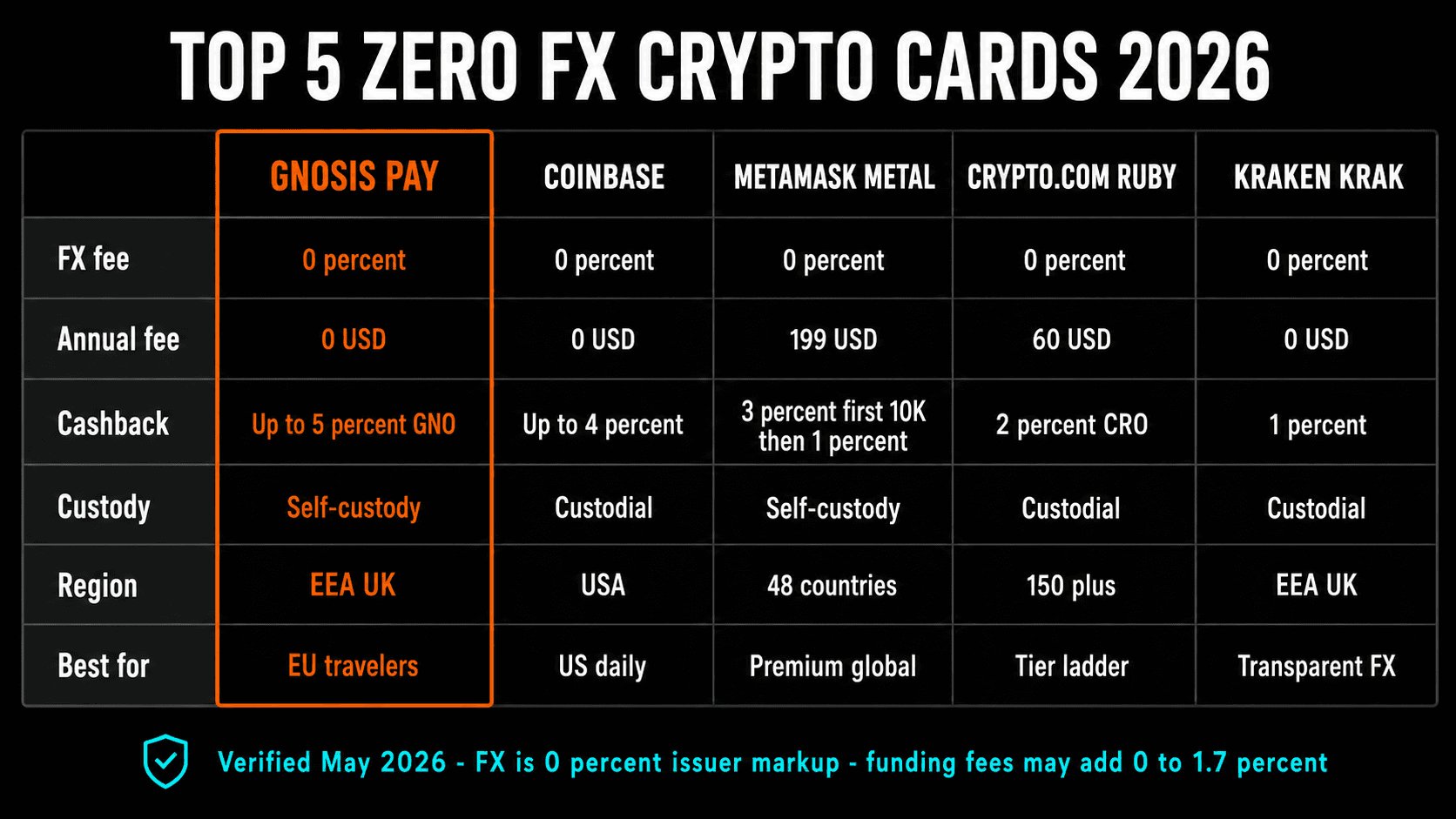

1. Gnosis Pay Card — Best Self-Custody Zero FX (EEA/UK)

Gnosis Pay is the strongest free self-custodial card in Europe. Your EURe stablecoin sits in a Safe Smart Account you control. 0% FX, 0% transaction fee, 0% gas, 0% off-ramp. Cashback ranges from 1% base up to 5% in GNO (Gnosis governance token) for stakers holding 10+ GNO (around $3,000 at current prices). EEA and UK only. The 30 EUR card setup is the only fee.

- Pro: True self-custody via Safe Smart Account, zero fees across the entire stack, EURe stablecoin avoids crypto-to-fiat conversion at swipe

- Con: EEA and UK only, 5% rate requires GNO staking, cashback is paid in GNO (volatile governance token)

- Best for: European crypto users who want self-custody and the lowest possible total cost

2. Coinbase Card — Best Zero FX in the US (Prepaid Visa)

Coinbase Card is the simplest 0% FX option for US residents. Funded from your Coinbase fiat balance (USD), so there is no crypto-to-fiat conversion fee eating into rewards. Rotating 4% crypto rewards in categories you choose in-app. $0 annual fee, $0 FX, FDIC-insured funds via Pathward. The simplest zero-cost 0% FX card on the US market.

- Pro: Zero fees of every kind, FDIC-insured funds, no crypto conversion since it pulls from USD balance, easy onboarding

- Con: US only, the 4% is rotating categories not flat, no self-custody option

- Best for: US travelers who want simplicity and FDIC protection

3. MetaMask Metal Card — Best Premium Self-Custody (48 Countries)

MetaMask Metal Card delivers 0% FX in 48 countries with 3% cashback on the first $10,000 spent annually (then 1%). At $199/year it is the premium option for global users who want self-custody outside Europe. MPC wallet, Mastercard rails, $30K/day spending limit. Available in the US, EEA, UK, Switzerland, and parts of Latin America. The Virtual tier is free but charges 1% cross-border, so only the Metal qualifies as a fully 0% FX product.

- Pro: Self-custody MPC wallet, 3% cashback on first $10K, premium metal physical card, broad regional availability

- Con: $199/year annual fee, cashback drops to 1% after the $10K cap, Virtual tier is NOT 0% FX

- Best for: Global users spending more than $830/month who want self-custody outside the EEA

4. Crypto.com Ruby and Above — Best Tier Ladder Zero FX

Crypto.com Card Ruby tier and above all run at 0% FX globally. Ruby requires a $500 CRO stake plus $60/year. Higher tiers (Royal Indigo at 3% cashback, Icy White at 4%, Obsidian at 5%) require larger CRO stakes. Works in 150+ countries — the widest global coverage of any 0% FX card on this list. Spotify rebate at Ruby tier effectively pays for the annual fee.

- Pro: Widest global coverage (150+ countries), Apple Pay and Google Pay support, tiered cashback ladder, mature platform

- Con: Requires CRO stake (volatile token, capital tied up), Midnight Blue free tier does NOT have 0% FX, custodial

- Best for: Existing CRO holders or travelers crossing many continents who want one card everywhere

5. Kraken Krak Card — Best Transparent Zero FX (EEA/UK)

The Kraken Krak Card runs at 0% FX, 0% ATM fees (no issuer fee at any ATM), 1% cashback, and $0 annual fee in the EEA and UK. Kraken shows exact conversion rates in-app, making it one of the most transparent cards for verifying your FX rate. UK users also get up to 3.6% APY via Krak Vaults. Modest cashback compared to the leaders, but unmatched on transparency and zero-fee simplicity.

- Pro: Genuine zero fees across the stack, in-app FX rate transparency, 3.6% APY on idle balances (UK)

- Con: EEA and UK only, 1% cashback is modest, no US availability

- Best for: European users who value rate transparency and zero-friction over peak cashback

The Three Traps That Burn Your 0% FX Savings

Even a card with a genuine 0% issuer FX markup can still cost money. Three places the cost hides:

Trap 1: Dynamic Currency Conversion (DCC)

DCC is when a foreign terminal asks: "Pay in EUR or USD?" If you select your home currency, the merchant's bank handles the conversion at a 5–8% markup. On a $5,000 trip, accepting DCC on every transaction costs $250–$400. That single prompt can wipe out an entire year of 0% FX savings.

Trap 2: Crypto-to-Fiat Conversion at Point of Sale

If your card funds from BTC or ETH, the issuer converts crypto to fiat at the swipe. The conversion spread is typically 0.5–1.5%, sometimes higher. On $15,000 per year of international spending, that's $75–$225/year of hidden cost on a card you thought charged 0%. The fix: fund with stablecoins (USDC, USDT, EURC) or fiat balance where supported.

| Funding Method | Conversion Fee | Best Cards for This Method |

|---|---|---|

| Fiat balance (USD/EUR/GBP) | 0% | Kraken Krak, Coinbase, Gemini |

| Stablecoins (USDC/USDT/EURC) | 0–0.2% | Gnosis Pay, MetaMask, XKard |

| Major crypto (BTC/ETH) | 0.5–1.5% | Crypto.com, Wirex |

| Altcoins | 1–3% slippage | Varies |

Trap 3: Per-Swipe Fees Labeled As Something Else

Some cards advertise 0% FX and then charge a separate per-transaction fee or conversion fee under a different label. Bitget Wallet charges a 1.7% conversion fee. Bitget Card charges 0.9% per swipe. These are not classified as FX fees, but the money leaves your pocket just the same. Always check total transaction cost against a Visa or Mastercard mid-market rate (use Google or XE.com) on your first few transactions to verify the real rate you are paying.

Real-World Net Savings at Three Spending Levels

The FX line is only one component. Annual fee, cashback, and conversion fees determine the actual net cost. Here is what each card nets you at three international spending levels.

| Card | $5K/yr Spend | $15K/yr Spend | $30K/yr Spend |

|---|---|---|---|

| Traditional bank (3% FX) | −$150 | −$450 | −$900 |

| Gnosis Pay (0% FX, 5% cashback) | +$250 | +$750 | +$1,500 |

| Coinbase (0% FX, 4%) | +$200 | +$600 | +$1,200 |

| MetaMask Metal (0% FX, 3% to $10K, $199 fee) | −$49 | +$151 | +$301 |

| Crypto.com Ruby (0% FX, 2%, $60 fee) | +$40 | +$240 | +$540 |

| Kraken Krak (0% FX, 1%) | +$50 | +$150 | +$300 |

Bottom line: at typical digital nomad volumes ($15K/year), the gap between a 0% FX crypto card and a 3% bank card is $1,200/year on Gnosis Pay or Coinbase. Even MetaMask Metal's $199 fee pays for itself at this level when you factor cashback on the first $10K.

Cards to Avoid for International Spending

Not every crypto card is a zero-FX card. Some popular cards charge meaningful FX fees that erase the "crypto card advantage" for travelers:

| Card | FX Fee | Cost at $15K/yr |

|---|---|---|

| BitPay | 3% | −$450 |

| Binance Card (where active) | 2% | −$300 |

| Ledger Card | 1.75% | −$263 |

| Bitget Wallet Card | 1.7% | −$255 |

| RedotPay | 1.2% | −$180 |

Some of these cards still make sense for non-international spending (Bitget Wallet's self-custody, Ledger's hardware integration, RedotPay's Asia coverage), but if more than 30% of your annual card spend is in foreign currencies, the FX fee will outweigh other perks.

Multi-Currency Wallet Strategy (Advanced)

Advanced travelers can eliminate even the interbank rate spread by pre-loading destination currencies:

- Before your trip, convert stablecoin balances to your destination currency (EUR, GBP, JPY) on a crypto exchange at wholesale rates.

- Load the fiat balance onto your card.

- Spend in the local currency directly from the matching fiat balance.

- No conversion happens at the point of sale.

Example: a Wirex user traveling Europe swaps $10,000 USDC to EUR at 0.1% fee ($10). During the trip, all EUR spending pulls from the EUR balance at zero conversion. Total FX cost: $10 on $10,000. A traditional bank card would cost $300 for the same volume. This strategy works on multi-currency cards (Wirex, Crypto.com). Cards with one base currency (Gnosis Pay in EUR, Coinbase in USD) still convert at point of sale, but at the interbank rate with 0% issuer markup.

Our Picks at a Glance

Best 0% FX card if you live in…

- EEA/UK: Gnosis Pay (self-custody, free, 5% cashback)

- US: Coinbase Card (4% rotating, FDIC-insured)

- 48-country global: MetaMask Metal

- 150+ countries, tier ladder: Crypto.com Ruby+

- Privacy + 0% FX: XKard

Skip for international spending:

- BitPay — 3% FX, same as a bank card

- Binance Card — 2% FX where active

- Ledger Card — 1.75% FX outweighs hardware perks

- Bitget Wallet — 1.7% conversion eats stablecoin savings

- MetaMask Virtual — 1% cross-border (only Metal is 0%)

Final Take

The most valuable 0% FX card is not the one with the lowest fees. It is the one where (annual cashback − annual fee − conversion costs + FX savings) nets out highest for your spending pattern. At $15,000/year international spending, Gnosis Pay (free, 5% cashback, EEA/UK) and Coinbase (free, 4%, US) deliver $600–$750/year in pure profit. A traditional bank card at 3% FX costs you $450/year on the same volume. The total swing is $1,050–$1,200/year.

Three habits will protect your savings: fund with stablecoins or fiat to avoid conversion fees, always pay in local currency to dodge DCC, and check total transaction cost on your first few foreign taps against a mid-market rate calculator. Do this and your travel spending earns money instead of burning it.