No-KYC Crypto Card Fees Compared: The True Cost of Privacy

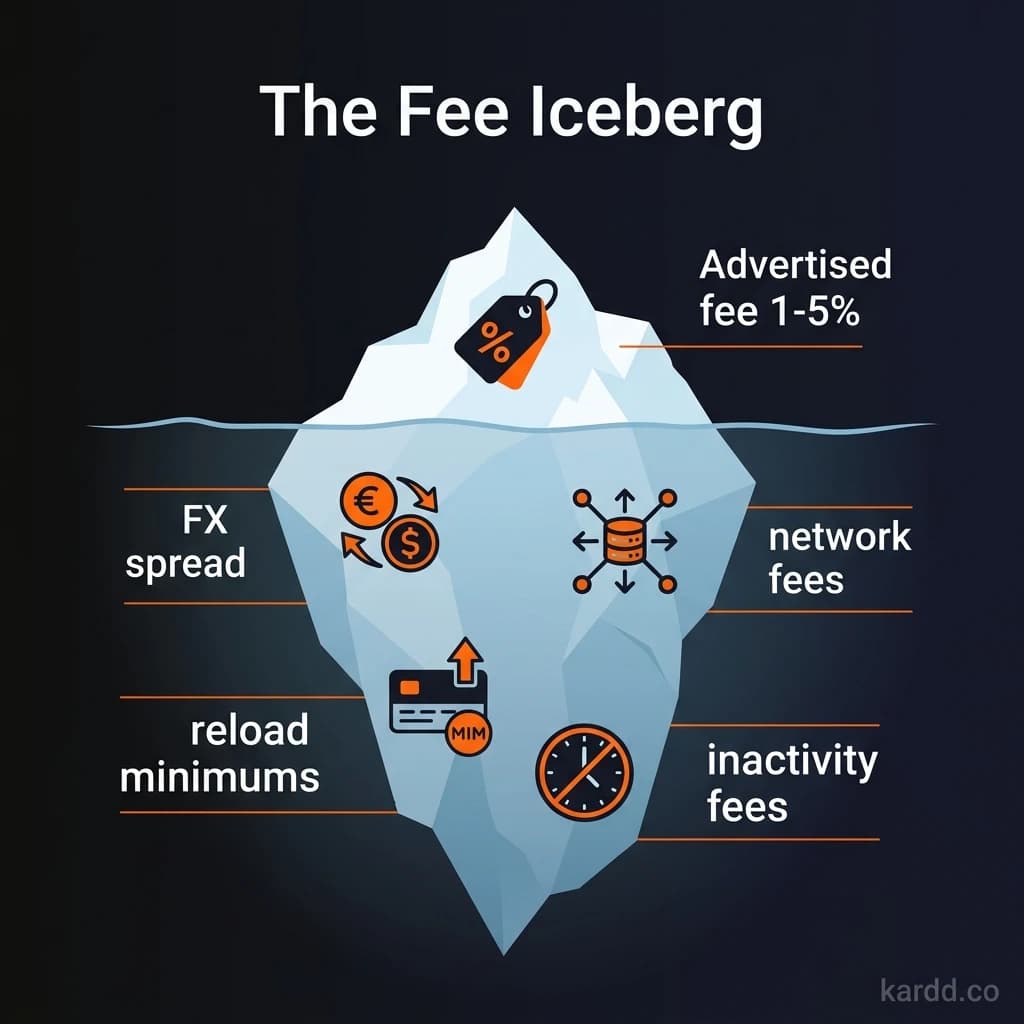

Every no-KYC crypto card advertises a single number — the top-up fee. But that number is a fraction of what you’re actually paying. Between exchange rate spreads, foreign currency charges, ATM fees, and annual subscriptions, the real cost of spending crypto privately is 2-3x what most users expect.

We broke down the complete fee structure for all 11 no-KYC crypto cards tracked on Kardd.co so you can see exactly what each dollar of crypto spending actually costs.

The Four Types of No-KYC Card Fees

Before comparing cards, understand the four fee layers that stack on every transaction:

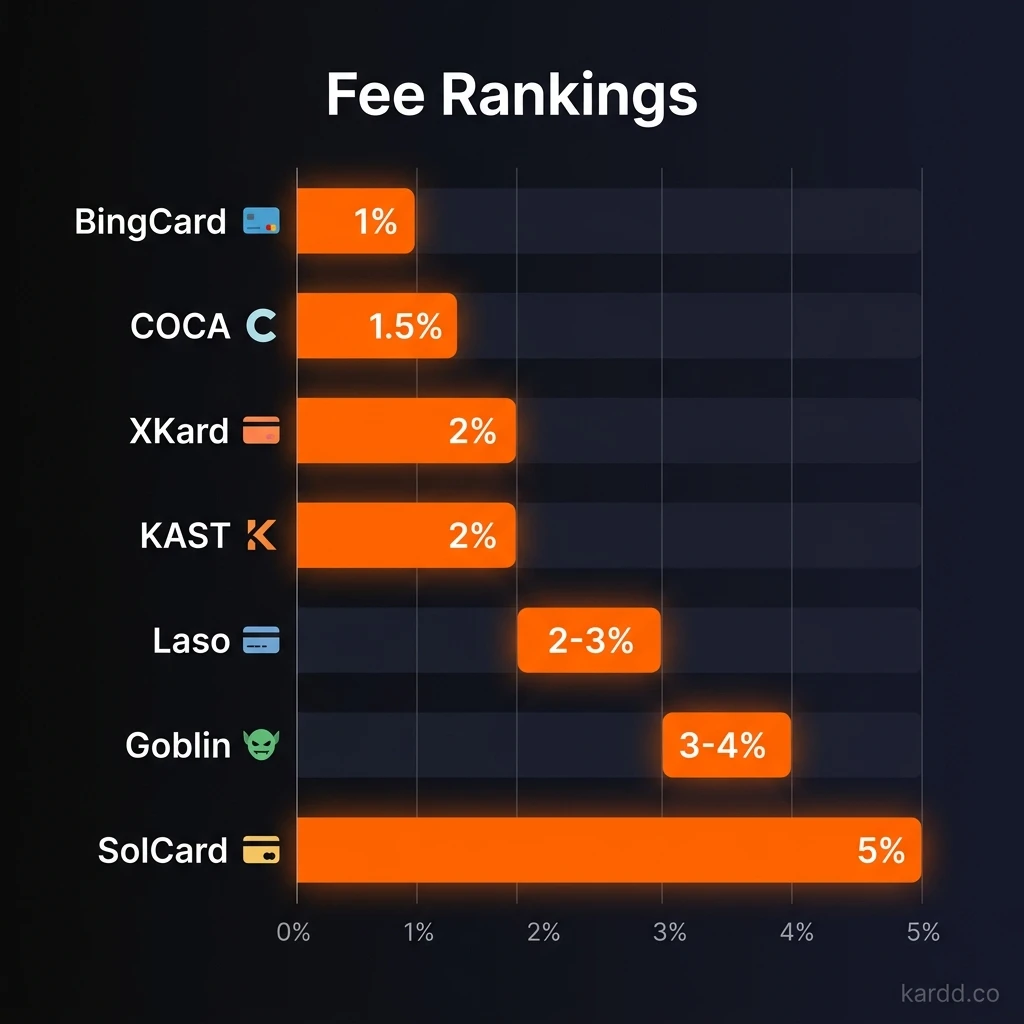

1. Top-Up Fee (1-5%)

Charged every time you load crypto onto the card. This is the headline number every card advertises. Ranges from 1% (BingCard) to 5% (SolCard).

2. Foreign Exchange Fee (0-2%)

If you’re spending in anything other than USD, most cards charge an FX markup. This hits European, UK, and Asian users hardest.

3. ATM Withdrawal Fee ($2-$5 flat)

Physical card holders pay a flat fee per ATM withdrawal. Virtual-only cards avoid this entirely.

4. Exchange Rate Spread (0.5-1.5% — hidden)

The invisible cost. When you load USDT, the card converts it to fiat at their rate — not the market rate. The difference goes to the provider and is never listed as a “fee.”

Full Fee Comparison Table

| Card | Top-Up Fee | FX Fee | ATM Fee | Annual/Monthly Cost | Est. Spread |

|---|---|---|---|---|---|

| XKard | 2.3-4.5% | 0% (USD) | $3.50 | $108-$588/yr | ~0.5% |

| BingCard | 1% | 1.5% | $2.50 | $79/yr | ~1% |

| SolCard | 5% | 2% | N/A (virtual) | Free | ~0.5% |

| Laso Finance | 2-3% | 1% | N/A (virtual) | $9.99/mo | ~1% |

| KAST | 2% | 1.5% | $4 | $99/yr | ~0.8% |

| Goblin Card | 3-4% | Unknown | $5 | Free | ~1.5% |

| Bancus | 2.5% | 1% | N/A (virtual) | Free | ~1% |

| COCA Card | 2.5% | 0.5% | $3 | Free | ~0.8% |

| Bitsika | 2% | 1.5% | N/A (virtual) | Free | ~1.2% |

| Bitget Wallet | 1-2% | 1% | N/A | Free | ~0.5% |

| Coinsbee | 0-5% | N/A | N/A | Free | Varies |

The Hidden Fee Nobody Talks About

Exchange rate spreads deserve their own section because they’re the most misunderstood cost in the no-KYC card space.

Here’s how it works: You load 1,000 USDT onto your card. The market rate for USDT/USD is $1.000. But the card provider credits you $985-$995 — not the full $1,000. That $5-$15 difference is the spread, and it’s on top of the stated top-up fee.

Why it matters: On a card with a 2% top-up fee and a 1% spread, your real cost is 3% — not 2%. Over a year of $2,000/month spending, that hidden 1% costs you $240.

Which Cards Have the Lowest Spreads?

- XKard and Bitget Wallet Card consistently show the tightest spreads (~0.5%)

- Goblin Card has the widest (~1.5%)

What Does a $1,000 Monthly Spend Actually Cost?

Here’s the total real cost per $1,000 in monthly spending (USD transactions, no ATM):

| Card | Top-Up | Spread | Annual Fee (monthly) | Total Monthly Cost |

|---|---|---|---|---|

| BingCard | $10 | $10 | $6.58 | $26.58 |

| Bitget Wallet | $10-20 | $5 | $0 | $15-25 |

| KAST | $20 | $8 | $8.25 | $36.25 |

| XKard (Standard) | $23-45 | $5 | $9-49 | $37-99 |

| XKard (Whale @ $10K) | $230 (2.3%) | $50 | $49 | $329 (3.29%) |

| Laso Finance | $20-30 | $10 | $9.99 | $39.99-49.99 |

| COCA Card | $25 | $8 | $0 | $33 |

| Bitsika | $20 | $12 | $0 | $32 |

| SolCard | $50 | $5 | $0 | $55 |

| Goblin Card | $30-40 | $15 | $0 | $45-55 |

Cheapest No-KYC Cards by Use Case

Under $1,000/month (casual spending):

→ BingCard — 1% top-up, cheapest total cost. No mobile pay.

$1,000-$5,000/month (regular spending):

→ XKard — 2.3-4.5% but with Apple Pay, Google Pay, and higher limits. Best all-around value.

$5,000+/month (high volume):

→ XKard Whale — Effective rate drops with volume. $100K monthly limit.

Non-USD spending (Europe, UK, Asia):

→ XKard (0% FX) or COCA Card (0.5% FX) — Avoid SolCard’s 2% FX fee.

Maximum anonymity regardless of cost:

→ Goblin Card — Most expensive (3-4% + high spread) but supports Monero and has no annual fee.

Why Do No-KYC Cards Charge More?

Three structural reasons:

1. Regulatory Risk Premium

Operating without full KYC means higher compliance costs, more chargebacks, and the constant threat of card network termination. Providers price this risk into fees.

2. No Economies of Scale

KYC cards like Crypto.com serve millions of verified users. No-KYC providers are smaller, with higher per-transaction overhead.

3. Limited Payment Network Leverage

Visa and Mastercard charge higher interchange rates to programs with anonymous users. Those costs pass to you.

The result: you’re paying a 1-4% premium for privacy compared to fully verified alternatives. Whether that’s worth it depends on how much you value spending without identity documents on file.

FAQ

What’s the cheapest no-KYC crypto card?

BingCard at 1% top-up fee is the cheapest for users spending under $1,000/month. For higher volumes, XKard’s effective rate of ~2.8% on the Whale tier is more cost-efficient due to $100K limits and mobile pay support.

Are there any no-KYC crypto cards with zero fees?

No. Every card has some fee structure — top-up fees, spreads, or annual charges. Cards advertising “no fees” typically have wider exchange rate spreads that cost you 1-2% invisibly.

Why does SolCard charge 5% when others charge 1-2%?

SolCard’s 5% top-up fee reflects its position as a Solana-native card with zero KYC and full Apple Pay + Google Pay support. The combination of zero verification, mobile pay, and SOL ecosystem integration commands a premium.

How can I minimize fees on a no-KYC card?

Three strategies: (1) Choose a card with low top-up fees for your volume tier, (2) Spend in USD to avoid FX charges, (3) Use Kardd.co to compare current fees — they change frequently.

Conclusion

No-KYC crypto card fees range from roughly $15 to $90 per $1,000 spent — a 6x difference depending on which card you choose. The headline top-up fee is only part of the story. Exchange rate spreads, FX charges, and annual subscriptions stack up fast.

The right card depends on your volume and use case. Compare all 11 cards on Kardd.co to find the cheapest option for your specific spending pattern. If you want AI-driven analysis to compare any product before buying, tools like Sentimyne can break down real user sentiment across reviews.

Cards Mentioned in This Guide

Last verified: March 18, 2026. Fees, spreads, and card terms may change without notice. Always verify current terms directly with the card issuer before loading funds. Full affiliate disclosure