Crypto Card Europe Under MiCA 2026: 8 Cards That Survived The Rules

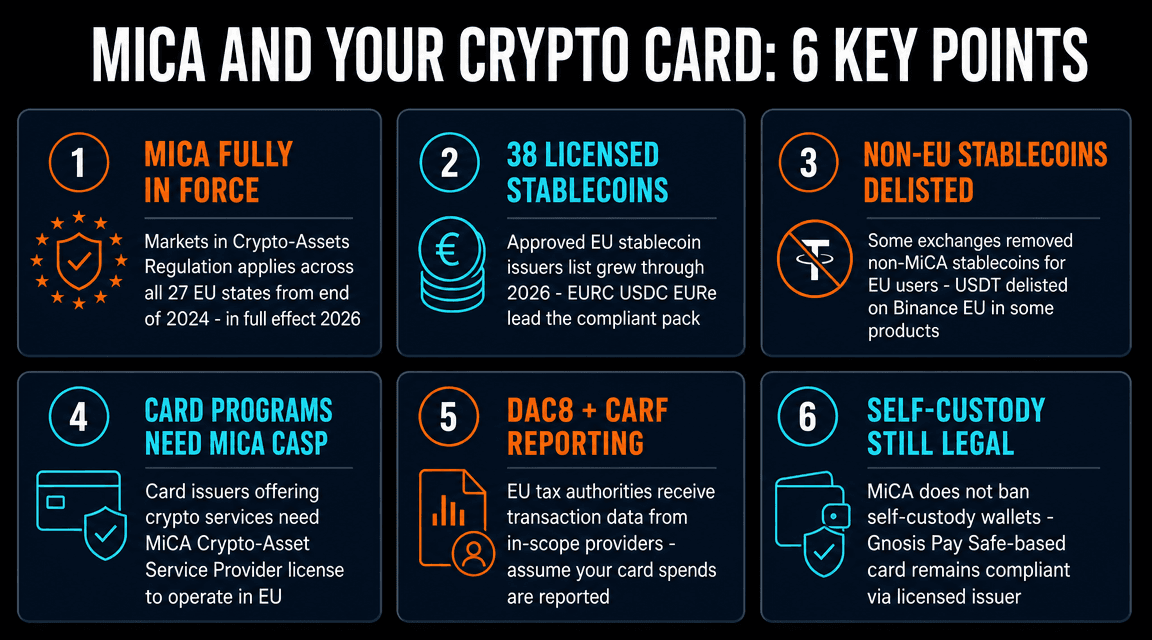

Quick answer: MiCA is fully in force across the EU in 2026. Stablecoin and asset-referenced token rules entered into force June 2024; the full CASP regime applied from December 2024. Crypto cards that survived and now operate compliantly for EU residents: Gnosis Pay (self-custody Safe, EURe via Monerium, EEA-licensed EMI partner), Bleap (self-custody, EURC, EEA), MetaMask Card (via Baanx EMI), Crypto.com Card (CASP authorized), Wirex, and XKard. USDT has been delisted on several EU exchanges (not banned for self-custody). DAC8 tax reporting from regulated providers begins 2026 — assume card activity is visible to your local tax office and report capital gains accordingly.

MiCA is now the most consequential crypto regulation any major economy has ever passed. The Markets in Crypto-Assets Regulation harmonized rules across all 27 EU member states. The stablecoin and asset-referenced token rules entered into force in June 2024. The full Crypto-Asset Service Provider (CASP) regime applied from December 2024. By 2026, the regulation is in steady-state enforcement — and the crypto card market has reshaped around it.

Some cards exited the EU. Some stablecoins got delisted on EU exchanges. New compliance paths emerged. This guide covers what MiCA means for crypto card users in 2026, the 8 cards confirmed available to EU residents under the new regime, and the regulatory friction points (DAC8 tax reporting, Travel Rule, KYC tier tightening) that didn't exist a year ago.

6 Things MiCA Changed for Crypto Card Users

- Card issuers running custodial crypto programs need MiCA CASP authorization. A "CASP" is a Crypto-Asset Service Provider, the regulated entity license under MiCA. Crypto.com obtained CASP authorization in Malta and France in 2024-2025. Kraken authorized in Ireland. Bitstamp in Slovenia. Cards operating in the EU without CASP authorization (or via a passported partner) cannot legally market to EU residents.

- Only MiCA-compliant stablecoins can be marketed to EU retail. Stablecoins fall into two MiCA categories: E-Money Tokens (EMTs, pegged 1:1 to a single fiat) and Asset-Referenced Tokens (ARTs, pegged to a basket). Both require authorization from a national competent authority. Approved EMTs as of 2026 include EURC (Circle), EURe (Monerium), USDC (Circle, dual US/EU authorization), and several bank-issued EU stablecoins.

- USDT delisted on multiple EU exchanges. Tether did not obtain MiCA authorization for USDT. Binance EU delisted USDT spot pairs in early 2025. Kraken, Coinbase, and Bitstamp have followed selectively for EU users. You can still hold USDT on self-custody wallets and bridge across non-EU chains, but on-EU-exchange on-ramping has become harder.

- DAC8 tax reporting from January 2026. The EU's Directive on Administrative Cooperation 8 extends automatic tax information exchange to crypto-asset service providers. In-scope CASPs report transaction data to your home tax authority. Card top-ups, on-ramps, and off-ramps via regulated EU providers are reportable. Assume your card activity is visible to your tax office.

- Travel Rule applies to crypto card top-ups over EUR 1,000. Transfers from one CASP to another over EUR 1,000 must include originator and beneficiary information. For card users this rarely matters — you're topping up your own card from your own exchange account — but if you're sending stablecoins from a non-EU service to fund an EU card, expect KYC friction.

- Self-custody remains legal and unregulated. MiCA explicitly excludes peer-to-peer transfers and self-custody from its scope. Cards built on self-custody (Gnosis Pay, MetaMask Card, COCA, Bleap) continue to operate — the regulated entity is the EMI or bank-of-issue settling the EUR leg, not your wallet.

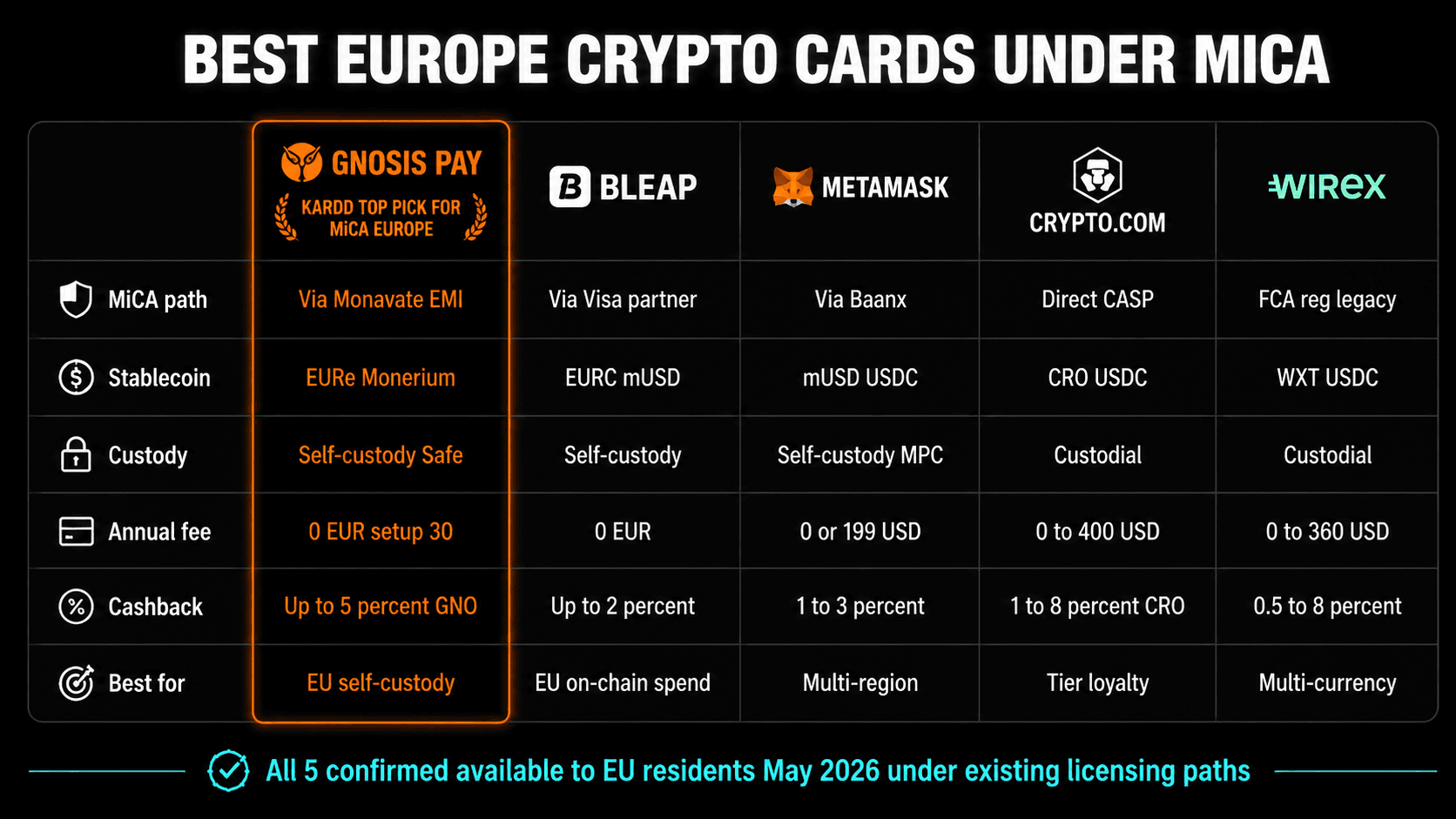

Top 5 Crypto Cards for EU Residents Under MiCA (2026)

1. Gnosis Pay Card — Best Self-Custody EU Card

Gnosis Pay is the strongest MiCA-era self-custody card in the EU. EURe (Monerium-issued EMT, MiCA-compliant) sits in a Safe Smart Account you control. 0% FX, 0% transaction fee, 0% gas, 0% off-ramp. Cashback 1% base, up to 5% in GNO for 10+ GNO stakers. The Monerium EMI license is passportable across the EEA. Card setup cost EUR 30 one-time, no annual fee. EEA and UK only.

- Pro: True self-custody via Safe Smart Account, MiCA-compliant EURe, zero fees across the stack, EEA-wide via Monerium passporting

- Con: EEA/UK only, EURe-only funding (no USDC at swipe), no ATM access, cashback in volatile GNO token

- Best for: European crypto users who want self-custody, zero-fee on-chain EUR spending, and the simplest MiCA-clean path

2. Bleap — EEA Self-Custody With Visa Rails

Bleap (bleap.finance) is an EEA-licensed self-custody card with EURC/mUSD funding. Built on Visa rails via a partner EMI. 0% FX, up to 2% cashback (capped). Free card. The Spanish-issued Bleap was one of the first cards to fully restructure for MiCA compliance — the card-issuing partner is MiCA-authorized and the supported stablecoins are EMT-authorized.

- Pro: Self-custody, fully MiCA-compliant stack, Visa rails, free, supports both EURC and mUSD

- Con: EEA only, cashback capped, smaller user base, no ATM access in some regions

- Best for: EEA users who want a fully MiCA-clean self-custody Visa

3. MetaMask Card — Self-Custody Mastercard via Baanx EMI

MetaMask Card launched EEA and UK in 2025 via Baanx (the EMI-licensed card-issuing partner). MPC wallet self-custody, Mastercard rails, 48 countries. Free Virtual tier with 1% mUSD cashback; Metal tier $199/yr with 3% on first $10K then 1%, zero FX. The Baanx partnership handles MiCA-compliant settlement; your funds stay self-custodial in MetaMask until swipe.

- Pro: Self-custody MPC wallet, Mastercard rails, broad country support, premium Metal tier, EEA/UK fully compliant

- Con: Metal tier expensive at $199/yr, Virtual tier has 1% cross-border (only Metal is 0% FX), cashback in mUSD requires gas-paid claim

- Best for: Active crypto users in the EEA/UK who want self-custody with Mastercard acceptance

4. Crypto.com Card — First Major CASP-Authorized Crypto Card

Crypto.com Card was among the first major exchanges to obtain MiCA CASP authorization (Malta, France, others). Free Midnight Blue tier. Ruby ($60/yr) and above unlock 0% FX and 1–5% CRO cashback. Apple Pay and Google Pay support. Direct EUR funding via SEPA. The mature platform option for EU users who don't need self-custody.

- Pro: MiCA CASP authorized in multiple member states, mature platform, direct SEPA EUR funding, Apple/Google Pay, tier ladder up to 5% cashback

- Con: Custodial (Crypto.com holds your balance), CRO stake required for higher tiers (volatile token), free tier does NOT have 0% FX

- Best for: EU users who prioritize platform maturity and tier ladder rewards over self-custody

5. Wirex — FCA-Legacy + Multi-Currency

Wirex operates in the EU under legacy FCA registration and EU-passported EMI agreements. Multi-currency accounts (USD/EUR/GBP) make it useful for cross-border spenders. Standard tier free, Premium $16.99/month, Elite $31/month. Cashback paid in WXT. Long-standing operation but the regulatory pathway is the most complex of the picks — verify status in your specific country before signup.

- Pro: Multi-currency accounts, mature platform, legacy FCA pedigree, broad EU availability

- Con: Custodial, cashback in WXT (volatile), monthly fees on higher tiers, MiCA pathway less clean than newer CASP-authorized competitors

- Best for: EU users who travel often and want a multi-currency hub card

What MiCA Actually Changes for EU Cardholders

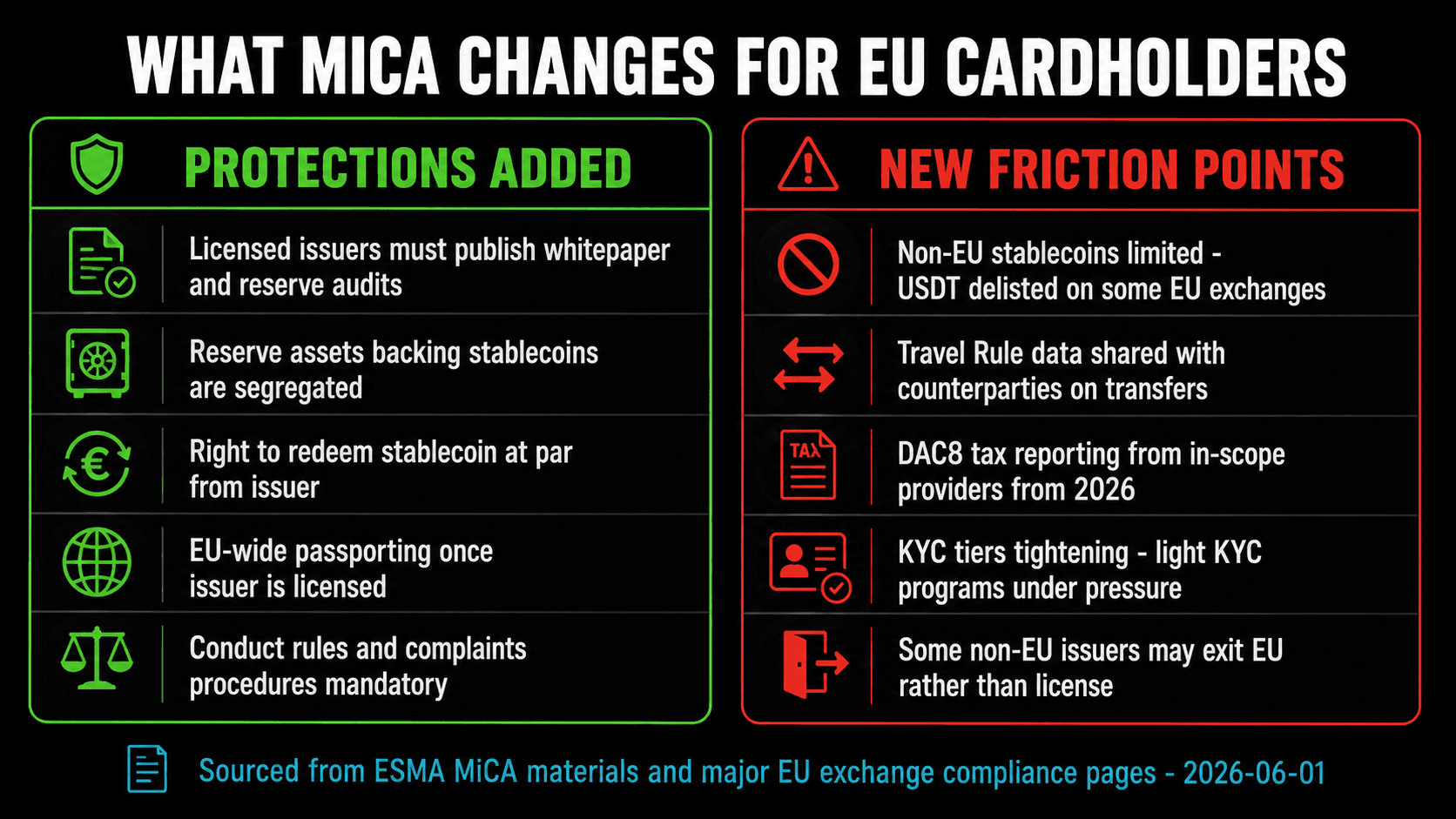

MiCA is not a ban — it's a framework that adds both protections and friction. Here's the practical impact for crypto card users:

Protections added

- Licensed issuers must publish whitepapers and reserve audits

- Stablecoin reserves are segregated from issuer assets

- Right to redeem stablecoins at par from the issuer

- EU-wide passporting once licensed in one member state

- Conduct rules and complaints procedures are mandatory

- Capital and prudential requirements for CASPs

New friction points

- USDT delisted on several EU exchanges

- Travel Rule data shared with counterparties > EUR 1,000

- DAC8 tax reporting from in-scope providers from Jan 2026

- KYC tiers tightening — light-KYC programs under pressure

- Some non-EU issuers exiting rather than getting licensed

- Stablecoin daily transaction caps under some EMI rules

The USDT Question

Tether did not obtain MiCA stablecoin authorization. The practical result: USDT trading pairs have been delisted on several EU-licensed exchanges (Binance EU early 2025, others selectively). You can still hold USDT in self-custody wallets and spend it via cards that accept USDT funding directly — MiCA does not regulate self-custody. But on-ramping EUR → USDT through a regulated EU exchange has become friction-heavy. For card funding, prefer:

- EURC (Circle, MiCA-authorized EMT)

- EURe (Monerium, MiCA-authorized EMT)

- USDC (Circle, dual US/EU authorization)

- Bank-issued EU stablecoins (38 accredited issuers as of 2026)

DAC8 and Your Tax Obligations

DAC8 (Directive on Administrative Cooperation 8) extends automatic tax information exchange to crypto-asset service providers from January 2026. In-scope providers report your transaction data to your home tax authority. For card users this means:

- Card top-ups via regulated EU exchanges are reportable

- On-ramps (SEPA → crypto) and off-ramps (crypto → SEPA) via CASPs are reportable

- Custodial card platforms send your transaction history to the tax office

- Self-custody activity is NOT directly reportable (DAC8 targets providers, not users), but on-chain forensics make it traceable

Cards That Exited or Restricted EU Access

MiCA did push some cards out of the EU market. As of mid-2026:

- Binance Card — suspended in EEA in 2023 (pre-MiCA) and has not relaunched under MiCA

- BitPay Card — never had meaningful EU presence; no MiCA pathway

- Some virtual-only no-KYC programs — couldn't meet EMI/CASP requirements and exited or restricted KYC tiers

- Several stablecoin-funded cards — either obtained CASP licensing or restricted access to EEA users only via partner EMIs

- Some Asia-Pacific cards — never expanded to EU formally; available via VPN but unsupported

Cards that successfully restructured for MiCA compliance kept the lights on by partnering with already-licensed EU EMIs (Monerium, Baanx, Quicko, etc.) rather than seeking direct CASP authorization themselves. This pattern (card-issuer + EMI partner) is now the dominant EU operating model.

Funding Your EU Crypto Card in the MiCA Era

The cleanest path for most EU users in 2026:

- On-ramp via a MiCA-authorized exchange. Kraken, Coinbase, Bitstamp, Bitvavo, and Crypto.com are CASP-authorized in at least one member state. Bank transfer (SEPA Instant) is the cheapest fiat rail.

- Buy MiCA-compliant stablecoins. EURC, EURe, or USDC. Avoid USDT for card funding through EU exchanges where it remains available — some platforms are scheduling further delistings.

- Withdraw to the chain your card uses. Gnosis Pay: EURe on Gnosis Chain. MetaMask Card: USDC on Linea/Base/Solana. Bleap: EURC on Polygon. Crypto.com Card: handled in-platform.

- Confirm before spending. Most chains confirm in under 30 seconds. Check the card balance in the issuer's app before your first tap.

Our Picks at a Glance

If you live in the EU and want…

- Self-custody EUR: Gnosis Pay

- Self-custody Visa: Bleap

- Self-custody Mastercard: MetaMask Card

- Mature platform + cashback ladder: Crypto.com

- Multi-currency travel: Wirex

- Privacy + light KYC: XKard

Skip in the EU:

- Binance Card — not available in EEA

- BitPay — no meaningful EU presence

- USDT-funded programs — on-ramp friction will worsen

- Cards routing via non-EU EMIs — verify license before signup

- Any program promising "no KYC ever" — will be CASP-non-compliant

Final Take

MiCA didn't kill crypto cards in the EU — it reorganized the market. The cards that survived (and several new entrants) are now operating with regulatory clarity that didn't exist a year ago. Stablecoin reserves are audited. EMI partners are licensed. Conduct rules are mandatory. For users this means a slightly less wild but materially safer environment.

For most EU residents in 2026, the right move is Gnosis Pay Card (free, self-custody, EURe, up to 5% cashback) or MetaMask Card (Mastercard rails, self-custody, broader country support). If you don't need self-custody, Crypto.com Card Ruby or above remains the cleanest CASP-authorized custodial option with mature SEPA funding. Whatever you pick: assume DAC8 reporting is in effect, track every crypto-to-EUR disposal for capital gains, and prefer MiCA-compliant stablecoins (EURC, EURe, USDC) over USDT for funding.