Virtual vs Physical No-KYC Crypto Cards: Which Should You Choose?

No-KYC crypto cards come in two forms: virtual (digital-only) and physical (plastic card shipped to you). The right choice depends on how you spend, where you spend, and how much you value anonymity.

Here’s the full breakdown.

Virtual Cards: What You Get

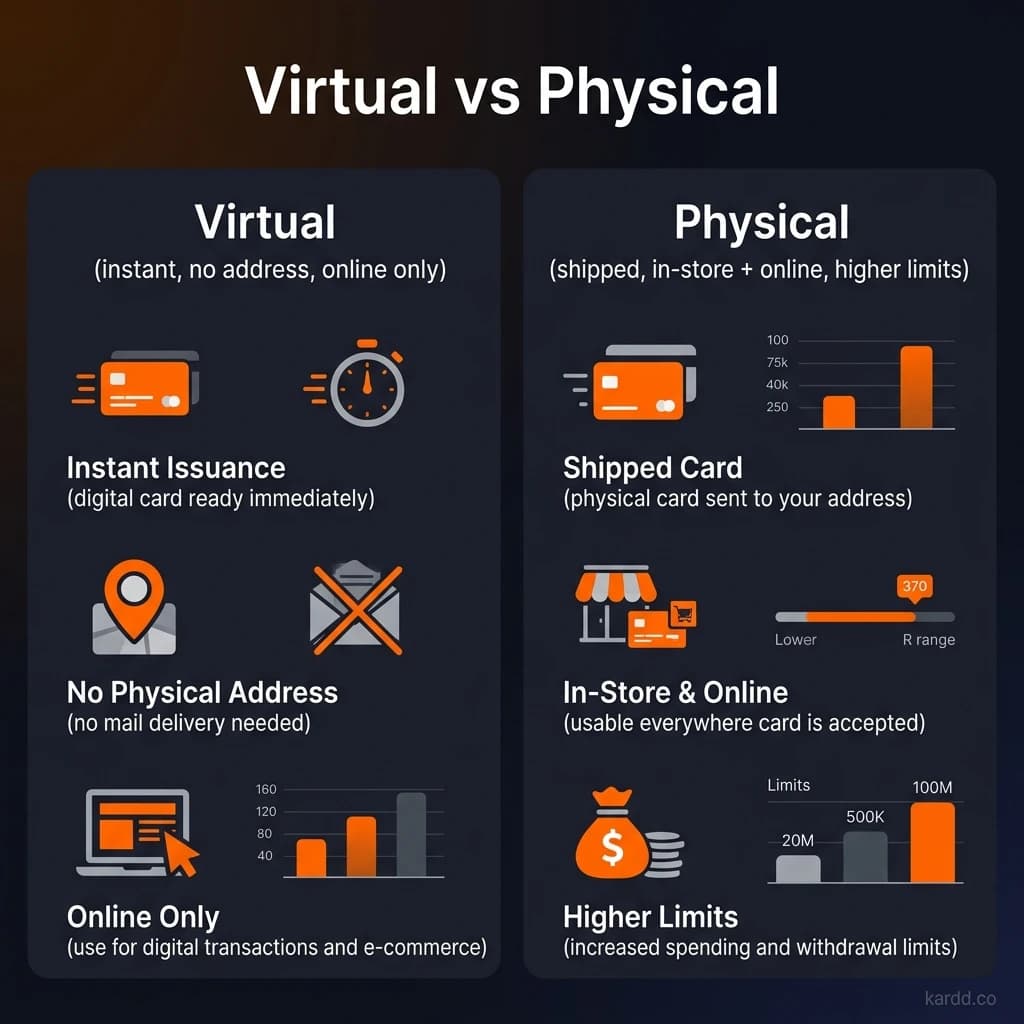

A virtual no-KYC crypto card is a digital card — card number, expiry date, and CVV visible in your online dashboard or app. No plastic. No shipping.

Advantages

- Instant issuance. Available in seconds after signup.

- Maximum privacy. No shipping address required. Nothing physical to trace.

- Works with Apple Pay and Google Pay. Tap-to-pay at NFC terminals via your phone.

- Online shopping. Enter card details at any checkout that accepts Visa/Mastercard.

- No card to lose or steal. Exists only in your dashboard and mobile wallet.

Limitations

- No ATM access. Can’t withdraw cash.

- No chip/PIN transactions. Some terminals require a physical card insert.

- Dependent on phone. In-store payments require Apple Pay/Google Pay compatible device.

Physical Cards: What You Get

A physical no-KYC crypto card is a plastic Visa or Mastercard shipped to an address. Works in-store via tap, chip, or magnetic stripe, plus ATMs.

Advantages

- ATM withdrawals. Convert crypto to cash at any ATM worldwide.

- Works everywhere. Chip/PIN, contactless, magnetic stripe — covers every terminal type.

- No phone needed. Pay in-store without a smartphone.

- Cash access. Important in regions or businesses that don’t accept cards.

Limitations

- Requires a shipping address. This is a privacy trade-off — someone knows where you are.

- 5-14 day wait. Not instant. You’ll wait for delivery.

- Can be lost or stolen. Physical risk. Replacement takes time.

- Shipping fee. Most charge $10-$30 for delivery.

- ATM fees. $2-$5 per withdrawal on top of card fees.

Head-to-Head Comparison

| Factor | Virtual Card | Physical Card |

|---|---|---|

| Setup time | Instant (seconds) | 5-14 days (shipping) |

| Privacy | Higher (no address needed) | Lower (shipping address required) |

| Online shopping | Yes | Yes |

| Apple/Google Pay | Yes (if card supports it) | Yes (plus standalone tap) |

| ATM withdrawals | No | Yes ($2-$5 fee) |

| Chip & PIN terminals | No | Yes |

| Risk of loss/theft | None (digital) | Yes (physical object) |

| Shipping cost | $0 | $10-$30 |

| Replacement | Instant reissue | Ship new card (5-14 days) |

Which No-KYC Cards Offer Virtual Only?

| Card | Type | Apple/Google Pay |

|---|---|---|

| SolCard | Virtual only | Yes (Both) |

| Laso Finance | Virtual only | Yes (Both + Samsung) |

| Bancus | Virtual only | No |

| Bitsika | Virtual only | No |

| Bitget Wallet | Virtual only | Google Pay |

Which Offer Both Virtual and Physical?

| Card | Physical Card Fee | ATM Fee |

|---|---|---|

| XKard | Included in subscription | $3.50 |

| BingCard | ~$15 shipping | $2.50 |

| KAST | ~$20 shipping | $4 |

| Goblin Card | ~$25 shipping | $5 |

| COCA Card | ~$15 shipping | $3 |

When to Choose Virtual

You should choose a virtual card if:

- You primarily shop online. Amazon, subscriptions, SaaS tools, food delivery — virtual covers all of it.

- You have Apple Pay or Google Pay. Your phone becomes your card. Tap to pay in-store works identically to a physical card at NFC terminals.

- Privacy is your top priority. No shipping address means one fewer data point connecting you to the card.

- You want instant access. Card ready in seconds, not days.

- You don’t need ATM cash. If you never withdraw cash from ATMs, a physical card has no advantage.

Best virtual-only picks:

- XKard — Zero KYC, Apple+Google Pay, up to $100K/month (also has physical option)

- SolCard — Zero KYC, both mobile wallets, Solana native

- Laso Finance — All three mobile wallets (Apple, Google, Samsung)

When to Choose Physical

You should choose a physical card if:

- You need ATM access. Converting crypto to cash requires a physical card. No workaround.

- You travel frequently. Some countries and merchants still require chip/PIN. Mobile pay acceptance varies by region.

- You want a backup payment method. Phone dies? Physical card still works.

- You operate in cash-heavy economies. Parts of Southeast Asia, Africa, and Latin America where card readers may not support NFC.

Best physical card picks:

- XKard — Physical included in subscription. Best limits ($100K) and mobile pay.

- Goblin Card — Physical card, zero KYC, accepts Monero. Best for privacy maximalists who also need ATM access.

- KAST — Physical + Apple Pay. Solid middle ground.

FAQ

Can I get both virtual and physical versions of the same card?

Yes — cards like XKard, BingCard, KAST, and COCA Card issue a virtual card instantly and optionally ship a physical card. Both share the same balance and limits.

Is a virtual card less secure than a physical card?

Actually more secure in most ways. A virtual card can’t be physically stolen, skimmed at a compromised terminal, or lost. The main risk is if your card dashboard/account is compromised — use a strong password and unique email.

Do virtual cards work at all in-store terminals?

Only at NFC (tap-to-pay) terminals via Apple Pay or Google Pay. They won’t work at chip-insert-only or magnetic-stripe-only terminals. In developed markets (US, EU, UK, Australia), NFC coverage is 90%+. In developing markets, coverage varies.

Can I withdraw cash with a virtual card?

No. ATM withdrawals require a physical card. If you need cash access, get a card that offers both virtual and physical options, or use Coinsbee gift cards as an alternative cash-out method.

Conclusion

For most users in 2026, a virtual card is the better choice — instant, more private, and works everywhere via mobile pay. Physical cards only win if you need ATM cash or travel to regions with limited NFC support.

Compare virtual and physical options

See which cards offer virtual, physical, or both — with full fee breakdowns.

Compare on Kardd.coCards Mentioned in This Guide

Last verified: March 18, 2026. Card details, fees, and KYC requirements may change without notice. Always verify current terms directly with the card issuer before loading funds. Kardd.co is an independent comparison site — we are not affiliated with any card issuer except through publicly available affiliate programs. Full affiliate disclosure