Your crypto, your rules. But finding a debit card that actually lets you spend USDT, USDC, or SOL without handing over your passport? That is harder than ever in 2026.

Regulators are tightening the screws. Card networks demand compliance. And half the “no KYC” cards from last year have either frozen funds, added verification, or disappeared entirely.

This guide cuts through the noise. We have tested, compared, and verified every no-KYC and minimal-KYC crypto card still operating in March 2026 — so you do not have to risk your funds finding out which ones actually work.

What Does “No KYC” Actually Mean for Crypto Cards?

Not all “no KYC” claims are created equal. Here is the reality in 2026:

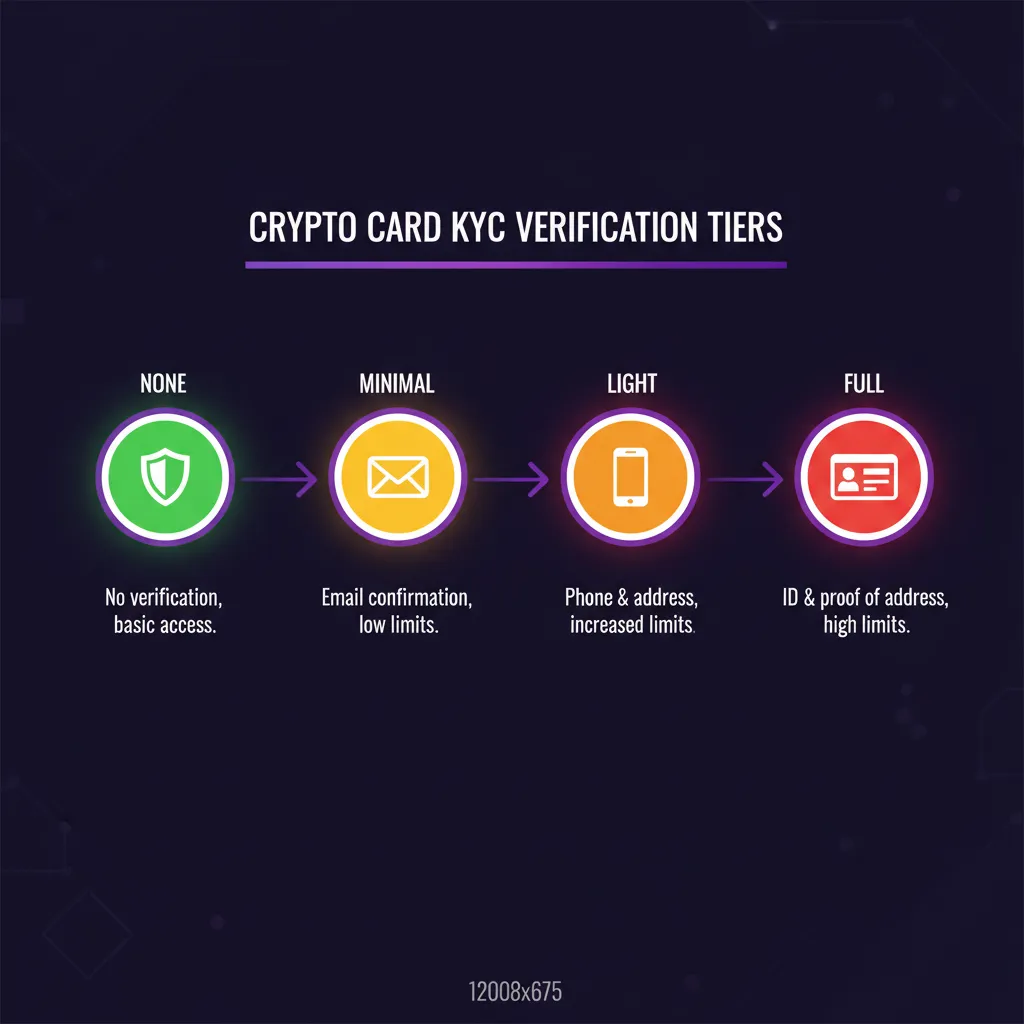

The Four KYC Tiers

None (Zero-Knowledge)

No personal info required. Email-only signup. No ID, no selfie, no address. Cards like XKard operate here.

Minimal

Email + phone number. SMS verification but nothing more. No documents, no facial recognition.

Light

Basic info (name, country) but no document upload. May escalate to full KYC at spending thresholds.

Full

Government ID, selfie verification, proof of address. What privacy-conscious users want to avoid.

The Corporate Issuing Loophole

How do these cards exist if Visa and Mastercard require KYC? Most no-KYC card issuers use corporate card programs. Instead of issuing a card in your name, they issue cards under a corporate entity. You are essentially using a sub-account on a corporate card — which does not trigger the same individual KYC requirements.

This is legal but exists in a grey area. It is why:

- Cards can disappear suddenly when issuers lose their banking partners

- Spending limits tend to be capped (to manage risk)

- Some cards have quietly added KYC after launching without it

Bottom line: “No KYC” does not mean “no rules.” It means the issuer has found a structure that does not require your identity — for now.

Top No-KYC Crypto Cards Compared (March 2026)

XKard — The Privacy Powerhouse

XKard is our number one pick for a reason. Zero personal information required, broad network support, and three pricing tiers that scale with your spending:

| Plan | Annual Fee | Reload Fee | Best For |

|---|---|---|---|

| Essential | $108/yr | 4.5% | Casual spenders (<$2K/mo) |

| Premium | $228/yr | 3.5% | Regular users ($2K-10K/mo) |

| Whale | $588/yr | 2.3% | High-volume ($10K-100K/mo) |

The math: If you spend $5,000/month, the Premium plan costs you $228 + ($5,000 x 12 x 3.5%) = $2,328/year. That is a 3.9% effective rate. Expensive compared to a bank card, but you are paying for privacy.

Watch out: Cross-currency fees can push total costs to 8-10%. If you are loading USDT but spending in EUR or GBP, factor in the conversion spread.

SolCard — The Solana Native

| Fee Type | Amount |

|---|---|

| Top-up fee | 5% |

| Foreign transaction | 2% |

| Monthly fee | Free |

| Card issuance | One-time fee |

Tier 2: Solid Alternatives

These cards offer good functionality with minimal KYC — email + basic info but no document uploads.

Laso Finance

The first no-KYC stablecoin prepaid card. Connect wallet, deposit, get a card.

BingCard

Issue a virtual card in 5 minutes without KYC. Physical card with verification.

COCA Card

Self-custodial wallet integration with card spending. Strong security model.

KAST

Solid virtual card option with competitive fees. Simple crypto-to-spending.

Fee Comparison: The Full Picture

Marketing pages love to hide fees. Here is what you will actually pay:

| Card | Annual Fee | Reload Fee | Foreign TX | Best For |

|---|---|---|---|---|

| XKard Essential | $108 | 4.5% | ~3-5% | Casual privacy |

| XKard Premium | $228 | 3.5% | ~3-5% | Regular spending |

| XKard Whale | $588 | 2.3% | ~3-5% | High volume |

| SolCard | Free | 5% | 2% | Solana users |

| Laso Finance | Varies | Varies | Varies | ERC-20 stablecoins |

| BingCard | Varies | Varies | Varies | Multi-crypto |

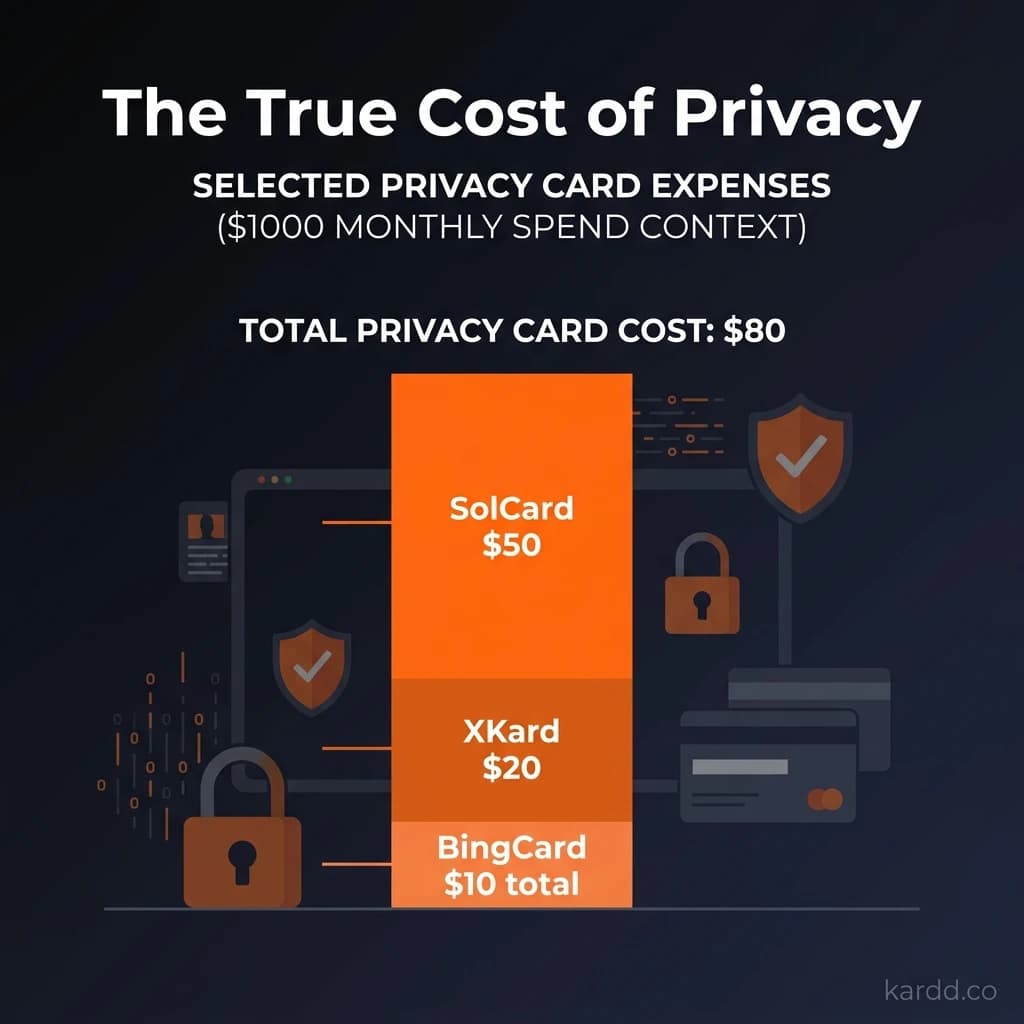

True Cost Analysis

At $1,000/month

Winner: SolCard

At $10,000/month

Winner: XKard Whale (saves $2,652/yr)

How to Choose the Right Card

Security and Privacy Considerations

Even “no KYC” cards collect something:

- Email address (all cards)

- IP address (all cards — use a VPN)

- Transaction history (stored by the issuer and payment network)

- Device fingerprint (when using Apple Pay or Google Pay)

Red Flags to Watch For

Best Practices

- Start small — Load $50-100 first and test a real purchase

- Use a burner email — Do not link your primary email to crypto cards

- VPN always — Mask your IP when loading and managing cards

- Do not store large balances — Load only what you plan to spend soon

- Screenshot everything — Transaction confirmations, support chats, card details

The Future of No-KYC Cards

The regulatory landscape is shifting fast:

- MiCA (EU) now requires identity verification for crypto-to-fiat above 1,000 EUR

- The Travel Rule is being enforced across more jurisdictions

- Corporate card loopholes are under increasing scrutiny

Our prediction: By late 2026, “no KYC” will be replaced by “minimal KYC” — email + phone as a baseline, with document-free tiers for lower spending limits.

If privacy in spending matters to you, now is the time to set up accounts while zero-knowledge options still exist.

The Bottom Line

| Need | Our Pick | Why |

|---|---|---|

| Best overall | XKard | Zero KYC, reliable, scales with volume |

| Cheapest for small spenders | SolCard | No annual fee, 5% flat |

| Best for ERC-20 stablecoins | Laso Finance | No KYC, instant issuance |

| Most crypto options | BingCard | BTC, ETH, USDT, USDC support |

Ready to compare?

Use our free comparison tool to see any cards side-by-side with full fee breakdowns.

Open Comparison ToolCards Mentioned in This Guide

XKard

Zero-KYC, Apple Pay & Google Pay, 15% affiliate

View full details →SolCard

Solana-native, virtual card, 40% referral

View full details →KAST

Minimal KYC, competitive fees, virtual card

View full details →BingCard

Zero KYC for virtual, BTC/ETH/USDT support

View full details →Laso Finance

No-KYC stablecoin prepaid, ERC-20 support

View full details →Last verified: March 18, 2026. Card details, fees, and KYC requirements may change without notice. Always verify current terms directly with the card issuer before loading funds. Kardd.co is an independent comparison site — we are not affiliated with any card issuer except through publicly available affiliate programs. Full affiliate disclosure