COCA Card Review 2026: Non-Custodial Visa, 8% Cashback in USDT, 6% APY

Our verdict: COCA Card is the most feature-dense crypto card in 2026 — combining a genuinely non-custodial MPC wallet, up to 8% USDT cashback within monthly allowances, 6% real DeFi yield via Morpho, 0% FX fees in 70 countries, and a personal EUR IBAN. The free Starter tier alone (1% cashback, 6% APY, 0% FX, no token staking) beats most paid competitor tiers. The trade-off: not available in the US/Canada, and higher tiers require staking $COCA — a small-cap token with real price risk.

COCA Card is a non-custodial Visa debit card issued by Wirex, built around a Privy-powered MPC smart wallet. You spend USDC, USDT, ETH, or BTC anywhere Visa or Mastercard is accepted, earn 1–8% cashback in USDT, and your stablecoin balance simultaneously earns 6% APY through Morpho lending markets. There is no annual fee. There is no FX fee. And unlike custodial competitors, COCA cannot move, freeze, or access your funds — you hold the keys.

We tested COCA Card across daily spending, Apple Pay, ATM withdrawals, and tier upgrades. Here is the full breakdown: features, all six tier mechanics, fees, the $COCA token risk, and how it compares to KAST, Crypto.com, Wirex, and MetaMask Card. Note: COCA is not available in the US or Canada as of May 2026.

What is COCA Card?

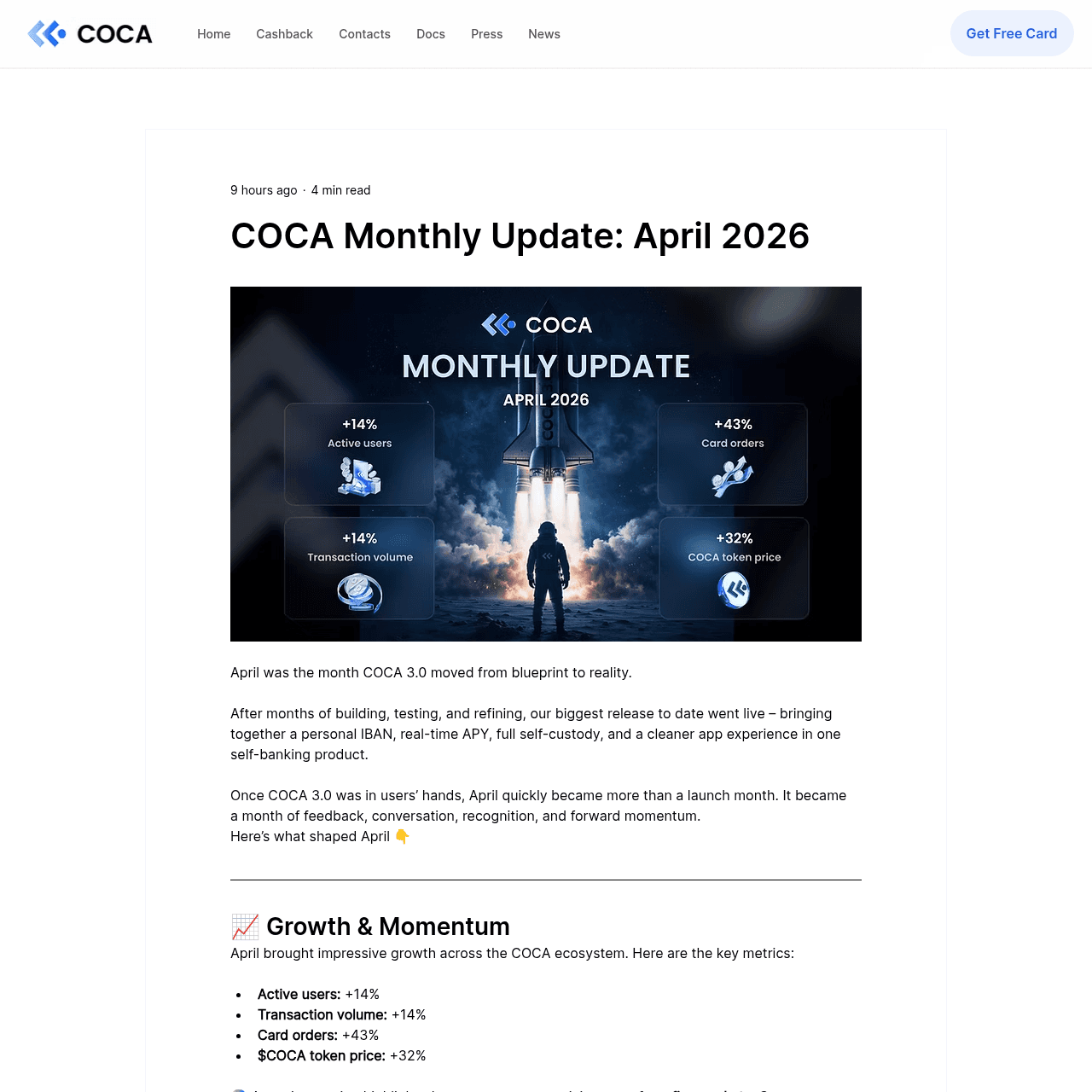

COCA started as a self-custodial wallet and evolved into a full self-banking app with the COCA 3.0 launch in April 2026. The card is issued in partnership with Wirex, the FCA-regulated UK fintech that has been operating crypto-fiat infrastructure since 2014. What makes COCA different from every custodial card on the market is the wallet architecture: your funds sit in a Privy-powered ERC-4337 smart contract wallet using MPC (Multi-Party Computation) cryptography — no seed phrase to lose, no exchange holding your assets.

The product reads like a feature dump until you actually use it: up to 8% cashback paid in USDT, 6% APY on stablecoin balances via real DeFi (Morpho lending, Gauntlet risk management), 0% FX fees on every currency, 50% rebates on Netflix/Spotify/ChatGPT/Amazon Prime, a personal EUR IBAN with SEPA transfers, and 50% off hotel bookings through COCA Travel. The 1M+ active users globally and recent COCA 3.0 momentum (+43% card orders, +14% transaction volume in April alone) suggest the product is finding its market.

Key Features

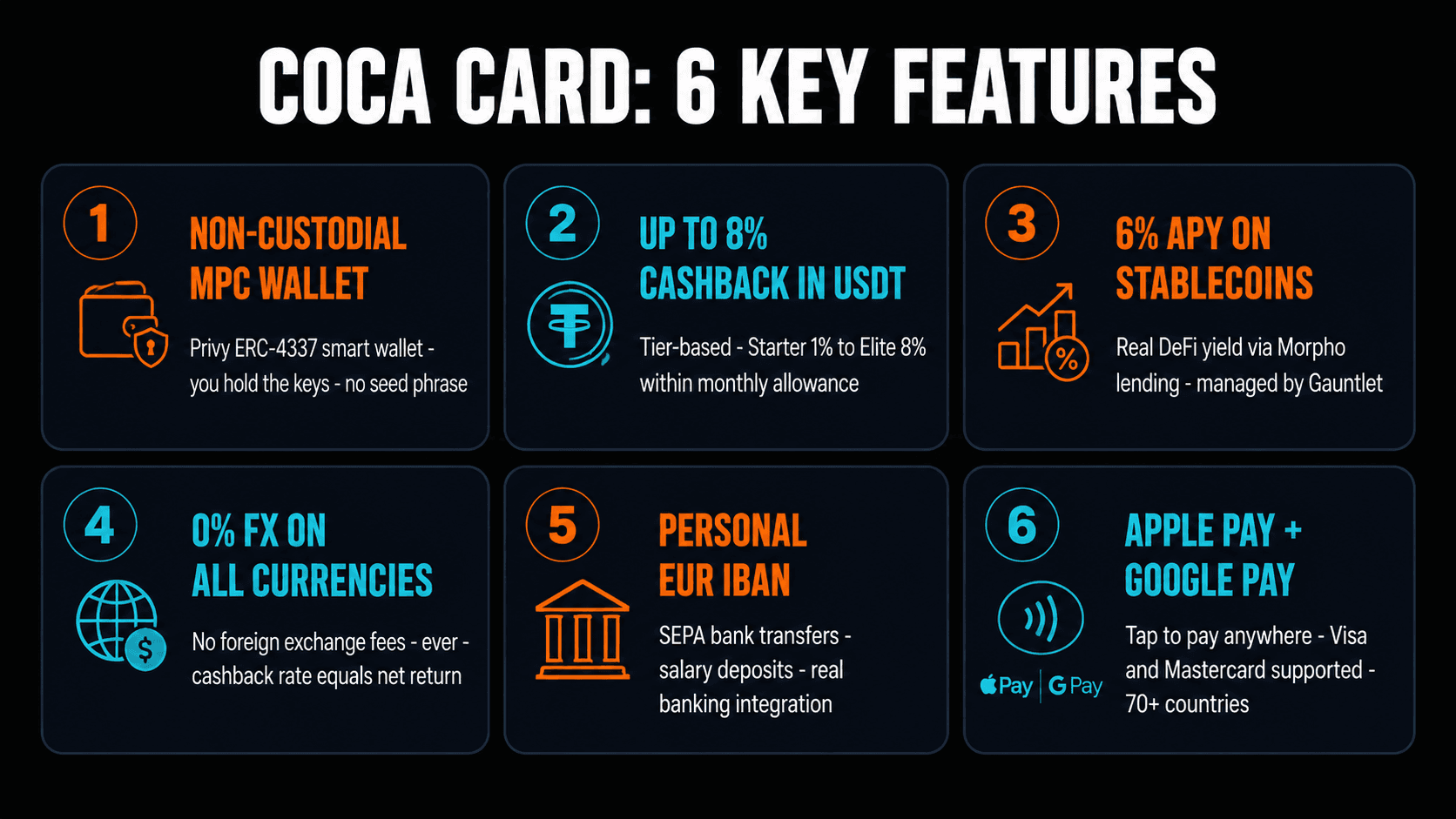

- Non-custodial MPC wallet. Privy-powered ERC-4337 smart contract wallet. SOC 2 Type I/II certified, audited by Cure53, Zellic, and Doyensec. Biometric recovery (no seed phrase), private key export available. COCA cannot access your funds — period.

- Up to 8% cashback in USDT. Tier-based: Starter (1%) through Elite (8%) within monthly allowances ($1K–$10K depending on tier). Above the allowance, all tiers earn 1%. Paid in stablecoin, not COCA token (changed Feb 2026).

- 6% APY on stablecoin balances. Real DeFi yield via Morpho lending markets, managed by Gauntlet. Tier-based balance caps ($5K Starter, unlimited Premium+ and Elite). Above the cap, you earn 2% APY. Calculated on minimum monthly balance, paid by the 10th of each month.

- 0% FX on every currency. No foreign exchange fees, anywhere. Your cashback rate equals your net return regardless of where you spend. This is rare in the crypto card market — even premium tiers at competitor cards charge 1–2% FX.

- Personal EUR IBAN. SEPA bank transfers built in. Receive salary directly, pay bills, move funds between accounts. Functions as a digital bank account, not just a crypto card.

- 50% subscription rebates. Netflix, Disney+, Paramount+, YouTube Premium (Standard tier and up), ChatGPT/Cursor (Standard+ and up), Spotify/Apple Music (Premium+ and up), Amazon Prime (Elite only). $70/month cap per service.

- COCA Travel. Up to 50% off hotel bookings and apartments through the COCA app.

- Apple Pay + Google Pay. Both Visa and Mastercard variants supported (Mastercard added April 2026 with COCA 3.0). 150M+ merchant locations, 70 countries.

All 6 Tiers Explained

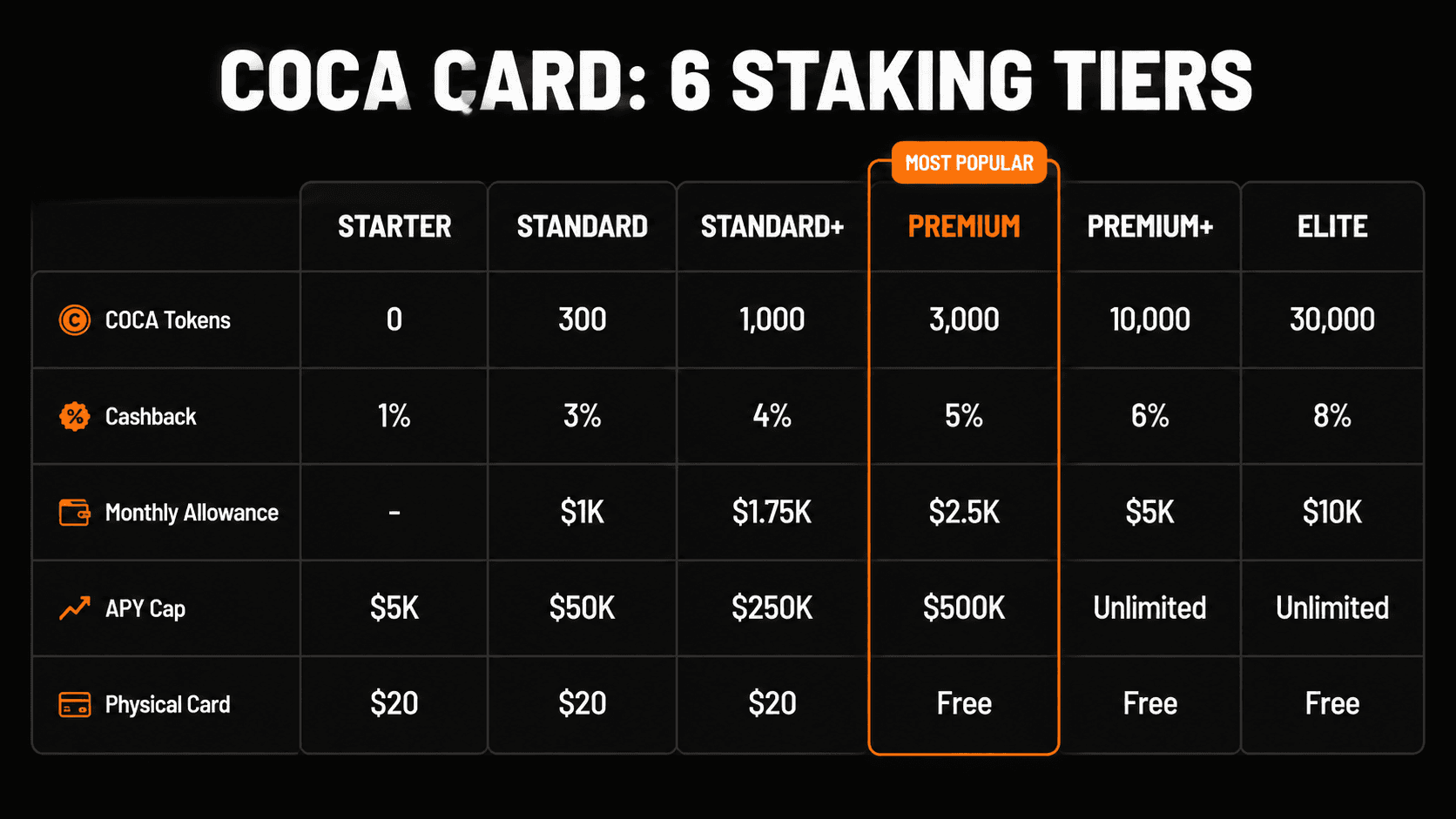

COCA's tier structure is the single most important thing to understand before signing up. Cashback rate, monthly allowance, APY cap, and subscription access are all gated by how many $COCA tokens you stake.

| Tier | $COCA Staked | Cashback | Monthly Allowance | APY Cap | Sub Rebates |

|---|---|---|---|---|---|

| Starter | 0 | 1% | — | $5K | None |

| Standard | 300 | 3% | $1,000 | $50K | 1: Video |

| Standard+ | 1,000 | 4% | $1,750 | $250K | 2: Video, AI |

| Premium | 3,000 | 5% | $2,500 | $500K | 2 + free card |

| Premium+ | 10,000 | 6% | $5,000 | Unlimited | 3: + Music |

| Elite | 30,000 | 8% | $10,000 | Unlimited | 4: + Marketplaces |

How tier staking works. Stake $COCA tokens in the COCA app to upgrade your tier. Staked tokens are locked for the duration of your tier membership — to unstake you cancel your tier (downgrades to Starter), wait a 30-day cooldown, then claim. No partial unstaking. Cancelling returns all staked COCA. Staking does not earn additional APY; staking is solely for tier access.

Above the monthly allowance, all tiers earn 1%. So Premium ($2,500/mo allowance at 5%) on $4,000 monthly spend = $2,500 × 5% + $1,500 × 1% = $140/month effective, not $200 you might assume from the headline rate.

Pricing & Fees

- Annual fee: $0 across all tiers

- FX fee: 0% on every currency

- Free ATM: $200–$250/month (varies by region), 2% above

- Virtual card: Free for all tiers, instant issuance

- Physical card: $20 for Starter/Standard/Standard+, free for Premium and above

- Crypto-to-fiat conversion: ~0.5% spread embedded in exchange rate (Visa network spread, not COCA fee)

- Top-up: Free via SEPA/IBAN, debit/credit card, or stablecoin deposit (network gas fees apply)

- Spending limits: EUR 30,000 per transaction/day/month, EUR 75,000 quarterly, EUR 100,000 semi-annual

Real-World Earnings: Three Scenarios

Starter ($2,200/month spend, 5K USDC balance)

At Starter (zero staking), 1% cashback on $2,200/month = $264/year. APY on $5K USDC at 6% = $300/year. Combined: $564/year, zero token risk, free card. This is the baseline that beats most paid competitors, and the math is simple: any spend you do is +1% pure profit since FX is 0%, and $5K parked stablecoins earn 6%.

Standard ($1,000/month spend, stake 300 COCA, $25K balance)

$1,000 × 3% = $360/year cashback (full tier rate within $1K allowance). APY on $25K at 6% (capped at $50K) = $1,500/year. 50% rebate on Netflix = ~$93/year. Combined: $1,953/year. Token cost at ~$1.30/COCA = ~$390 staked. Break-even: ~3 months.

Premium ($3,500/month spend, stake 3,000 COCA, $25K balance)

$2,500 × 5% + $1,000 × 1% (above allowance) = $1,620/year. APY on $25K = $1,500/year. ChatGPT + Netflix rebates ~$213/year. Combined: $3,333/year. Staked tokens worth ~$3,900 — earned back in <14 months.

The $COCA Token Risk

This is the single most important caveat. $COCA is a small-cap token trading at roughly $1.30 (April 2026), with an all-time high of $1.65 in January 2026 and a June 2025 low of $0.09. Token risk grows linearly with your tier:

- Starter: 0 tokens, 0 risk. The free tier is genuinely free and beats most competitor paid tiers.

- Standard (300 tokens): ~$390 exposure. A 50% drop costs you ~$195. With $1,080/year in extra cashback over Starter, this is recoverable in 6 months even after a 50% token crash.

- Elite (30,000 tokens): ~$39,000 exposure. A 50% drop costs you ~$19,500. To break even, you need rewards that exceed the depreciation. This only makes sense for users who have done their own analysis on $COCA fundamentals.

Important caveat: Cashback is paid in USDT (changed Feb 2026), so reward stability is not affected by $COCA token price. The risk is entirely on the staked principal. Mitigations: 30-day unstaking cooldown means you can exit if conditions change, private key export is available for your $COCA tokens, and the Starter tier provides full functionality with zero token exposure.

How To Get Started

- Download the COCA app — iOS, Android, or Telegram. Available in 70 countries (UK, EEA, APAC, LATAM).

- Create your non-custodial wallet — MPC setup via Privy. No seed phrase. Biometric recovery enabled by default.

- Complete KYC — identity verification through Wirex (required for card access). Wallet itself remains no-KYC.

- Choose your tier — start at Starter (zero tokens) for free 1% cashback + 6% APY. Upgrade if your spending math justifies the token stake.

- Fund and spend — deposit stablecoins via SEPA, card, or crypto. Add to Apple Pay or Google Pay. Spend anywhere Visa/Mastercard is accepted.

Pros & Cons

Pros

- Genuinely non-custodial via Privy MPC

- $0 annual fee on every tier

- 0% FX on every currency

- 6% APY via real Morpho DeFi yield

- Up to 8% cashback in USDT (stablecoin, not volatile token)

- Personal EUR IBAN with SEPA

- 50% subscription rebates at Premium+

- Apple Pay + Google Pay (Visa & Mastercard)

- Free Starter tier beats most paid competitors

- Issued by Wirex (11+ year track record)

Cons

- Not available in US or Canada

- $COCA token small-cap volatility risk at higher tiers

- Monthly allowance caps limit cashback at high spend

- 30-day cooldown to unstake tokens

- Stablecoin-only spending (BTC/ETH auto-convert)

- $20 physical card fee for lower tiers

- Newer track record than Crypto.com

- EUR IBAN only (no GBP or USD bank account yet)

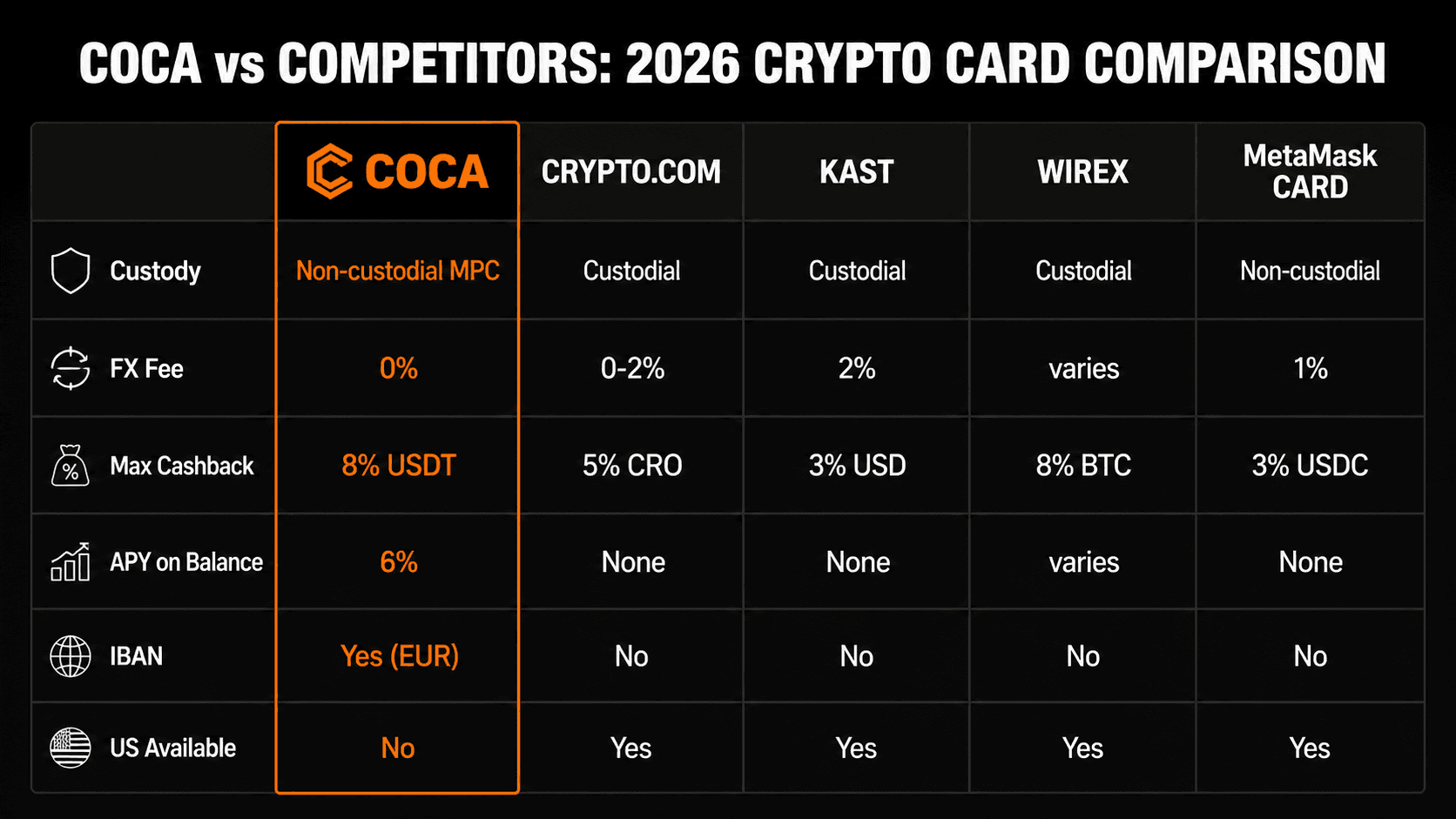

COCA vs Competitors

| Feature | COCA | Crypto.com | KAST | Wirex |

|---|---|---|---|---|

| Custody | Non-custodial MPC | Custodial | Custodial | Custodial |

| FX Fee | 0% | 0–2% | 2% | 0.5–2% |

| Max Cashback | 8% USDT | 5% CRO | 3% USD | 8% BTC |

| APY on Balance | 6% (Morpho) | None | SOL staking only | Varies |

| IBAN | Yes (EUR) | Limited | USD only | Yes |

| US Available | No | Yes | Yes | Yes |

Bottom line: If you are in a supported market (UK, EEA, APAC, LATAM), COCA Card wins on the combination of non-custodial architecture + 0% FX + APY + cashback. For US users, see KAST or Crypto.com. For maximum privacy without KYC, see our anonymous crypto card guide. For Web3-native funding from any wallet, COCA is also our top pick — see the Web3 cards comparison.

Final Verdict

COCA is the most feature-dense crypto card in 2026 and our top pick for non-custodial spenders in supported regions. The Starter tier alone (free, 1% cashback in USDT, 6% APY on $5K, 0% FX, free virtual card) is genuinely competitive with most paid competitor tiers. Stepping up to Standard or Premium unlocks meaningful uplift if your spending and stablecoin balance justify the token stake. Elite is for users who have done independent analysis on $COCA fundamentals and want to maximize the reward stack.

The headline risk is the $COCA token. Mitigations exist (30-day cooldown, USDT cashback, private key export, Starter tier with zero exposure), but anyone considering Premium+ or Elite needs to model token-downside scenarios. The other constraint is geography: if you are in the US or Canada, this card is not available — full stop.

FAQ

Is COCA Card non-custodial?

Yes. COCA uses Privy-powered ERC-4337 smart contract wallets with MPC (Multi-Party Computation) cryptography. You hold the keys; COCA cannot move, freeze, or access your funds. The card is issued in partnership with Wirex (FCA-regulated UK firm), but custody of stablecoins remains with you until the moment of spend. This positions COCA alongside Gnosis Pay in the genuinely non-custodial crypto card category.

Is COCA Card available in the US or Canada?

No. COCA is available in 70 countries across the UK, EEA, APAC, and LATAM regions. The card is regulated by Wirex's UK and EU licensed e-money institutions, and US/Canada are not currently on the supported list as of May 2026.

Does COCA require KYC?

For the wallet, no — COCA Wallet is fully non-custodial with no identity requirements. For the card, yes — Wirex requires identity verification (passport or government ID) to comply with EU/UK e-money rules. You can use the wallet without ever ordering a card.

Is the 6% APY real or subsidized?

Real DeFi yield. COCA pays 6% APY on stablecoin balances through Morpho on-chain lending markets, managed by Gauntlet (a risk-first vault curator). It is not promotional or subsidized. Tier-based balance caps apply ($5K Starter, $50K Standard, $250K Standard+, $500K Premium, unlimited Premium+ and Elite). Above the cap, you earn 2% APY.

What stablecoins does COCA Card support?

USDC, USDT, ETH, and BTC are the spendable assets, auto-converting to fiat at the moment of purchase. The COCA Wallet supports 15+ chains including Ethereum, BNB Chain, Polygon, Solana, and Stellar for top-ups, so you can fund from any major self-custodial wallet.

What is the $COCA token risk?

$COCA is a small-cap token (~$1.30 in April 2026, ATH $1.65, June 2025 low $0.09). Higher tiers require staking real $COCA at risk of price drops. Cashback is paid in USDT (since Feb 2026), so reward stability is unaffected — the risk is entirely on the staked principal. The Starter tier requires zero tokens and zero risk, so you can use COCA fully without any token exposure.

How long does it take to unstake COCA?

30 days. To unstake you cancel your tier (which downgrades you to Starter), wait the 30-day cooldown, then claim your tokens. Tier benefits continue during the cooldown period. No partial unstaking is supported.

Does the Starter tier really cost nothing?

Yes. Zero $COCA staked. $0 annual fee. Free virtual card. 1% cashback in USDT, 6% APY on up to $5K stablecoin balance, 0% FX on every currency, $200–$250/month free ATM withdrawals. The physical card costs $20 if you want one. This is one of the strongest free-tier crypto cards available in 2026.